The European TV Market

Western Europe is a mature market

for televisions and a challenging one for set makers who hope to entice consumers

to upgrade for the sake of new features.

by Bob Raikes

THE EUROPEAN TV MARKET is at the same time very simple and very complex. The big brands

are basically Korean and Japanese (Samsung, LG, Sony, Panasonic, Toshiba, and Sharp)

with the addition of a local brand, Philips, which is now controlled in the European

TV market by TPV of Taiwan under a joint venture with the Dutch company. Chinese

brands are doing some business, and there is a range of smaller brands run by TV

assemblers, traders, or retailers. The German market has a number of local companies

– Loewe, Metz, and Technisat – that offer "Made in Germany" sets that

are at the premium end of that market, and the Danish firm of Bang and Olufsen also

has a very high-end niche presence.

There has been no new brand in Europe that has been able to achieve the kind

of presence that Vizio has been able to achieve in the U.S. market. The particular

conditions that enabled Vizio to scale so quickly have not been present in Europe,

and the complications and high costs of operation in the market make it impossible

to achieve high volume quickly unless you simply "buy market share." Many have

tried and failed. Typically, they start well and then find that the cost base escalates

faster than the revenues.

Technical Requirements

The displays used in TVs in Europe are, of course, the

same as those used in the rest of the world. Sizes tend to be smaller than in some

other areas, which reflects small room sizes compared to that for the U.S., some

cultural issues about the importance of TV, and the relatively slow development

of HD services, which have only really become widespread in most of the major European

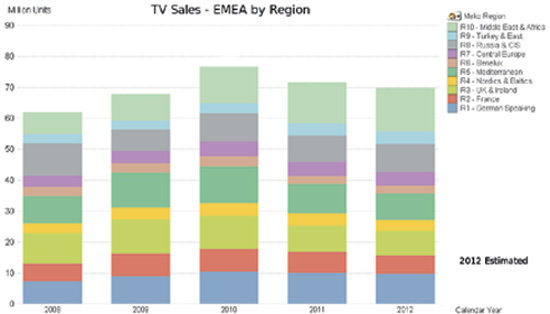

countries over the last year or two. Figure 1 shows an overview of TV sales by

region in EMEA (Europe, Middle East, and Africa).

Fig. 1: Overall TV sales

in Europe, the Middle East, and Africa (EMEA) appear to have peaked in 2010.

(Source: Meko.)

In addition, parts of Eastern Europe have a GDP per capita that is closer to

the developing world than the rest of Europe, and consumers simply cannot afford

a large set. Thirty-two inches remains the largest-size segment, although 40 in.

and above is growing. Philips said at IFA (see sidebar for more about the IFA consumer-electronics

show) this year that it believes that 46 in. will be mainstream in a couple of years.

Regarding the chassis of the TV, there is a big difference in the hardware and

software requirements to sell in all the markets in Europe. As well as the challenges

of language, the TV broadcast systems are different on a national basis. There

are differences in the balance among terrestrial (DVB-T and DVB-T2), satellite (mostly

DVB-S2), and cable (a mix of analog, DVB-C, and soon DVB-C2). There is also some

IPTV, with France the most developed market. Codecs are either MPEG-2 or MPEG-4

and there are different combinations of the broadcast standards and codecs for HD and SD in different countries.

Much broadcasting in Europe is government controlled and funded

by mechanisms including licensing, advertising, and combinations of these two.

There is plenty of pay TV, but the success of pay TV greatly varies from country

to country, and the key service providers are basically different in each one, although

some firms, including Sky and Canal Plus, operate in multiple countries. Liberty

Global is a cable operator in multiple countries. Satellite is regional, and the

broadcasting hardware is owned by SES and Eutelsat, but there are a number of different

service providers using that technology.

Content protection is an issue for the pay-service providers and,

again, there are a range of solutions, although for TV-set makers, the arrival of

the CI+ slot specification can allow the use of a standard TV and tuner to receive

encrypted content without a set-top box, providing the service provider decides

to support the use of an appropriate decryption [Conditional Access Module (CAM)]

card. Interactive technology is different around the region, with the UK and some

others basing systems on the license-free, public MHEG5 middleware, which is used

to control interactivity.

Broadcasters in France and Germany have developed a system for

hybrid services, combining traditional broadcast sources with Internet content.

That system, HbbTV (Hybrid Broadband Broadcast TV), is an open standard designed

to provide a business-neutral technology platform to blend TV services delivered

via broadcast with services delivered via broadband. HbbTV also enables access

to Internet-only services for consumers using connected TVs and set-top boxes.

The standard has rapidly developed support. However, despite the popularity of

HbbTV, the UK has launched its own "YouView" hybrid digital-TV service platform.

These complicated local conditions make it very hard to develop

a range of electronics and sets that can match the needs of the different markets

unless vendors have a very large share of the market or simply focus on one or two

countries. Getting a large share means a sales organization that can basically

sell at country level, which is expensive. The technical and sales overheads make

it hard for new and small brands.

European TV Supply Chain

The TV assembly and supply chain in Europe is based

in the countries that are just outside Germany. There is a 14% duty rate on TV

imports into Europe and this means that to be successful in anything but the smallest-sized

sets, one has to assemble them in Europe. The factories have moved from the UK,

Spain, Italy, and France to Hungary, Poland, Slovakia, and the Czech Republic.

Some panel makers have established module assembly plants to support the TV business.

Turkey has a special deal with the EU to allow TVs to be imported

from Turkey to EU countries without duty being levied, and Vestel of Turkey is a

major player in the worldwide OEM business. Vestel makes millions of TVs a year

in Turkey (it hopes to make 10 million this year) and supplies a number of the major

brands for at least parts of their ranges. The firm also assembles LCD modules

and uses the Finlux and Telefunken brands, among others. In 2011, it said that

it had made a total of 100 million TV sets in its history. Beko of Turkey is smaller,

but owns the Grundig brand and is more focused on its own brand.

Korea has a trade deal with the EU under which the duty on all

trade gradually disappears over the 5 years to 2016. However, both

LG and Samsung have developed strong vertical TV businesses based on local LCD-module

assembly in Poland and Slovakia. Because of this local investment, it seems unlikely

that these companies will change the structure because this would reduce their flexibility

and increase their inventories. There are import duties from Europe and other regions

into Russia, so Vestel is one of a number of companies that make TVs in that country.

At one time, NXP (previously Philips Semiconductors), Micronas,

and others made lots of chips for TV sets, but those two companies were acquired

by Trident of Taiwan, which itself went into Chapter 11 in January of this year.

So, there is no longer any substantial European interest in the TV-set chip market,

although STMicroelectronics makes chips for STBs and some TVs.

|

IFA: Europe's Premier Consumer

Electronics Show

The annual International Funkaustellung (International

Radio Exhibition) or IFA in Berlin is the annual event for the TV set, consumer

electronics (CE), and, in recent years, household appliance industry, in Europe.

It has a similar status in Europe to CES in North America.

IFA also has a special place in display history. Since the 1920s,

display-technology breakthroughs in the TV industry have been shown here, many for

the first time. The show also has a place in German political history. In the

period after 1945, when Berlin was occupied, and especially during the height of

the cold war, making the journey to support the people of Berlin at IFA was seen

as a matter of political support from the West for German brands.

Germany has a great tradition of trade shows, and more than 100,000

trade visitors attend the six days of IFA each year, along with more than 100,000

consumers. All the major brands in the consumer electronics world have significant

presences. Most of the big ones have one of the 28(!) halls to themselves.

The global TV industry has a very clear annual cycle that is quite

different from that of the IT world. At the Consumer Electronics Show (CES) in

North America in January, companies show the products that they expect to launch

on the market during the year. Shortly after that, they follow up with detailed

launch events for their dealer networks and press.

In Q2, the brands start to change over their product ranges to

"current year" models as they build toward the peak sales period – the day

after Thanksgiving or "Black Friday" in the U.S. in November, and Christmas and

New Year sales in Europe. The timing of the IFA consumer-electronics show in Berlin

at the beginning of September is not great for TV brands in terms of showing new

technology. Companies will do so, but they would prefer to focus in public on the

products that are in the stores now rather than risk the possibility that consumers

will defer their purchases until after the holidays.

As a result, many of the most interesting technology developments

are not shown publicly at IFA and that was true this year. The main innovations

were in 4K displays and in OLED TVs and these were the hot topics at CES back in

January as well, although I thought that there was a lot more emphasis on 4K at

IFA. (For more on the 4K and OLED TV market, see last month's Display Marketplace

and Industry News articles.) Still, IFA remains a great place to get a sense of

the industry and its trends.

– Bob Raikes

|

Market Forecasts

The market forecasts for Europe do not look very positive.

Western Europe is a very mature TV market and most set purchases are replacements.

The trend to increase the number of second sets has stopped, and second and third

sets are probably on the decline because of the wide adoption of tablets and other

devices for Internet-delivered TV viewing. Eastern Europe still has plenty of consumers

who would like to upgrade and modernize their sets, but the economies need to get

moving to enable this.

Although European consumers are very conservative, they can be

persuaded to spend money on features such as 3-D, 4K, or smart TV if they feel that

they need to be "upgrade proof." In recent years, the set makers have tended to

drive innovation faster than some of the more conservative buyers can really absorb the new features and so have not maximized the value they

could have achieved.

At last year's IFA, Meko's TV analyst described the kind of confusion

over 3-D, smart TV, HD, and other TV features as the "Perfect Storm" that could

allow a company that could offer a simple solution to make real inroads into the

market. That might be an opportunity for Apple, or someone else, but they would

have to deal with the complications of the broadcast environment. The TV is not

going away as the central entertainment center of the home, but the economic success

of TV brands will depend on the balancing of the simplicity and complexity that we have referred to earlier

and in providing just enough innovation for consumers to feel that they need to

upgrade the kind of set that they buy. •

Bob Raikes is a principal analyst with

Meko. He can be reached at bobr@meko.co.uk.