Tablets Impact the Notebook Market: Enter the Ultrabook

The tablet PC, in its short lifetime, has already influenced the mobile PC market in numerous ways, but none more concretely than in inspiring the emergence of the Ultrabook.

by Richard Shim

TABLET PCs have given consumers what they have been asking for from notebook and desktop PCs for years – convenience. At DisplaySearch, we describe the currently emerging era of computing as convenience computing, in which devices enable instant-on capability and all-day battery life in extremely portable form factors. Notebook and desktop PCs have made incremental advances in convenience computing over the years, but those products remain predominately performance-computing devices. Tablets are more oriented toward convenience and tablet makers (more specifically, tablet-maker Apple) have experienced tremendous success and shipment growth as a result (Fig. 1).

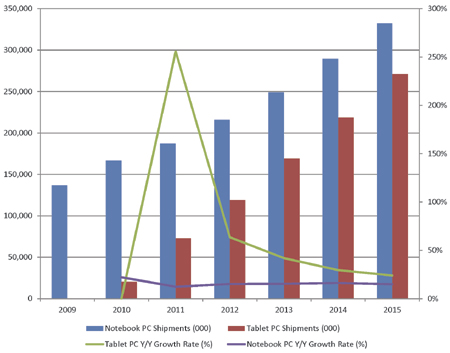

Fig. 1: Tablet sales increased spectacularly in 2011. While the rate of growth will not continue at 2011 levels, tablet shipments will continue to increase through at least 2015. Source: DisplaySearch.

The notebook market is not in decline, but the shipment forecast is not anywhere near as promising as that of the tablet market. In 2011, DisplaySearch estimates over 72.8 million tablets will ship, as compared to 187.5 million notebooks. By 2015, tablet shipments will reach 271.1 million units, as compared to 332.5 million notebooks. In response to the rapid growth of the tablet market, a new category of notebook is emerging that is supposed to offer the key features of a tablet – notably instant-on and all-day battery life – in a thin (thinner than that for conventional notebooks) form factor. Further down the road, we expect notebooks to take on characteristics found first in tablets, such as an app store and applications whose usefulness is tied to the Internet. The notebook is called the Ultrabook, and expectations are high that this product category can fulfill the current needs of consumers and compete with tablets. (Display industry members should note that other than thinner glass and design, Ultrabooks are similar to notebooks and are not expected to enable many new display characteristics at this point.)

One of the key beneficiaries of the rise of tablets is the ARM processor architecture developed by ARM Holdings. All tablets running Android, iOS, webOS, and QNX use ARM processors. These relatively simple but low-power-consuming processors are a good fit in tablets as well as smartphones, and their rise in popularity is a sign that high performance is not the only characteristic used to measure experience on computing devices.

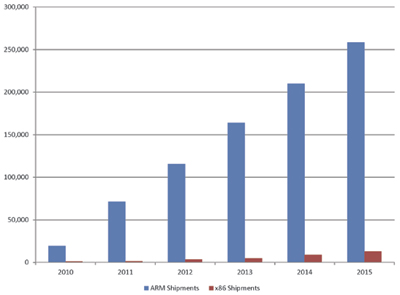

For 2011, DisplaySearch estimates over 71 million tablets using ARM processors will ship, and by 2015 that number is expected to increase to nearly 258.3 million units (Fig. 2). In 2011, no tablets running Android, iOS, webOS, or QNX are using ´86 processors and by 2015 DisplaySearch estimates less than 12.8 million tablets will be using 86 processors. Additionally, Microsoft is looking to make Windows 8 available on ARM and ´86 processors, and while Google is working on an Android OS version for the ´86 microarchitecture, it is in the early stages of development. This all makes ´86 chip-making-giant Intel nervous. There is clearly a hole in the market where ´86 is not yet tapping into the key needs of consumers (instant-on computing, all-day battery life, and extremely portable form factors). To address this market, Intel is promoting the Ultrabook.

Fig. 2: Shipments of tablets with ARM processors will far exceed shipments of tablets with ´86-based processors at least through 2015. Source: DisplaySearch.

While the rise in the popularity of tablets points to the rise in convenience computing, at the same time, convenience-oriented computing platforms are adding higher levels of performance capability. For example, current tablets already have dual core processors, and upcoming tablets are expected to offer multiple cores. The tablet platform is evolving to incorporate more performance capabilities and, similarly, the notebook platform is adopting more-convenience-oriented characteristics. The resulting computing platform that lies at the intersection of convenience and performance computing is the Ultrabook.

The Ultrabook Push

The role of ringleader among Ultrabook backers in large part belongs to Intel. Though Apple's MacBook Air can arguably be pointed out as the first notebook to fit the Ultrabook description, Intel has been working to define the category and to lower it from premium status to make it available to the mainstream market. Intel went as far as obtaining a trademark for the term Ultrabook so it can control who can use the term as well as benefit from the chip maker's Ultrabook marketing campaign. Being under the halo of Intel's marketing is very helpful, as Intel typically invests hundreds of millions of dollars in brands such as Centrino. However, fitting under the definition can be tough.

The Ultrabook experience is meant to enhance performance, response, security, form factor, and battery life compared to conventional notebooks, all at a price within reach of mainstream PC buyers. This is a tall order that will take time to be completely fulfilled. The Ultrabook definition is expected to evolve with several stages. The stages are dependent on price and the availability of key technologies. In many instances, the components needed are expensive, which will make it difficult to produce a product that is affordable to mainstream consumers.

For example, solid-state drives (SSDs) enhance the notebook experience on several levels, making them ideal for use in Ultrabooks, but there is a hefty price premium that puts them out of the realm of affordability for the mainstream market. As a result, the Ultrabook definition currently recommends SSDs but also allows for thin hard drives. Intel has announced that it will invest $300 million in various areas of the supply chain in which it can drive economies of scale to lower the price of premium components for use in Ultrabooks.

According to Intel's specifications, the current retail price point for Ultrabooks (notebooks using Intel's "Sandy Bridge" CPU, with more than 5 hours of battery life, a +Z height of less than 21 mm for units with screens larger than 14 in. and less than 18 mm for units with screens smaller than 14 in.) is less than $1000. In 2012, the price point should become lower – less than $700 for notebooks using Intel's "Ivy Bridge" CPU, having more than 8 hours of battery life, USB 3.0/Thunderbolt ports, and a Z height of less than 21 mm for units with screens larger than 14 in. and less than 18 mm for units with screens smaller than 14 in. By 2013, the price point becomes lower, less than $600, for notebooks using Intel's "Haswell" CPU, having more than 8 hours of battery life, USB 3.0/Thunderbolt ports, and a Z height of less than 21 mm for notebooks with screens larger than 14 in. and less than 18 mm for notebooks with screens smaller than 14 in. (Table 1).

Table 1: Ultrabooks, as defined by Intel, will become thinner and less expensive each year through 2013. Source: DisplaySearchQMPC Q4 '11 Shipment and Forecast Report.

| |

2011 |

2012 |

2013 |

| CPU |

Sandy Bridge |

Ivy Bridge |

Haswell |

| Z-Height |

<21 mm for >14 in. notebooks |

<21 mm for >14 in. notebooks |

<21 mm for >14 in. notebooks |

| <18 mm for <14 in. notebooks |

<18 mm for <14 in. notebooks |

<18 mm for <14 in. notebooks |

| Battery life> |

>5 hours |

>8 hours |

>12 hours |

| I/O |

|

USB 3.0/Thunderbolt |

USB 3.0/Thunderbolt |

| Retail price |

>$1000 |

>$700 |

>$600 |

Next to price, the challenge for Ultrabook makers is getting to the right Z-height requirement. As has always been the case in the notebook world, thinness and portability have mass appeal. Ultraportables, sub-notebooks, and even mini-notes/netbooks were appealing to consumers mainly because they were slim and lightweight.

For Ultrabooks, two methods of enabling the required thinness focus on the notebook lid. There are limits to how thin the base of a notebook can get, given the heights of ports such as VGA and Ethernet that are typically included in notebooks. By reducing the Z height of the lid, manufacturers and brands can get significantly closer to Intel's requirements.

One method of getting to thinner notebook lids involves using 0.4 mm or thinner glass panels. Currently, the demand for thin panels is relatively modest, and handling such thin panels requires sensitive equipment that can properly manage thin glass without breaking it. This has limited thin-panel production, but such production is on the rise. Currently, the major panel makers are committing on the order of single-digit percentages of overall production for thin notebook panels. However, consumer trends are increasingly pointing to a preference for thinner design, so we expect to see thin-panel production to rise, although wide availability for notebooks is not expected until 2015.

The other method to enable thinner notebook lids is LG Display's Shuriken solution. This method essentially streamlines the assembly process, eliminating the need for secondary front and bottom covers, not only reducing the thickness but removing some cost from the build of materials. Instead of the panel maker simply sending the device maker a finished panel to be added to the notebook production process, the panel maker and the device maker are more aware of each other's production plans. The panel maker sends the device maker a panel specifically for a notebook model. This helps to cut back the need for secondary front and bottom panel covers for use in the notebook lid. This method has its risks; in particular, single sourcing since LG Display is the only panel maker offering it. As far as incorporating non-mainstream display technologies to create thinner, more-cost-effective Ultrabooks, current plans do not exist for it because new screen technologies would add to the build of materials.

Reducing cost will be a central theme in Ultrabooks for the next couple of years and the reason is simple: notebooks over $1000 appeal to less than 15% of the addressable market. Currently, Apple owns the rarified air of price points above $1000, accounting for more than 50% of notebook shipments. However, that upper price echelon does not translate to high shipment volumes, which is what Intel is aiming for with Ultrabooks. Intel has stated a goal of 40% of premium consumer notebooks shipped at the end of 2012 to be Ultrabooks (Table 2).

Table 2: Ultrabook shipments are forecasted to increase aggressively through 2014. Source: DisplaySearch QMPC Q4 '11 Shipment and Forecast Report.

| |

2011

|

2012

|

2013

|

2014

|

| Ultrabook I |

3,413

|

16,842

|

34,911

|

57,101

|

The DisplaySearch forecast for Ultrabook shipments highlights the benefits of a device that offers the convenience of a tablet and the performance capabilities of a notebook. In the short term, the potential for Ultrabooks is going to be helped in late 2012 by the expected launch of Windows 8 and Intel's Ivy Bridge processor, but will be slowed by not having a full year of availability of either and by premium pricing of components, leading to high price points for the category. In 2013, Ultrabooks will be helped along by a full year of availability of Windows 8 and the expected mid-year release of Haswell. In 2014, we expect the Ultrabook platform to essentially be at full strength with Windows 8, the Haswell processor, and more opportunity to drive down costs and price points.

The Ultrabook represents the intersection of two competing computing platforms currently in the market; convenience versus performance computing. Devices representing the two platforms, tablets for convenience and notebooks for performance, are taking on the differentiating characteristics of the other. It is logical for the evolution of these platforms to cross because it is clear, based on the size of the market for each, that consumers want the best of both worlds. In the short term, the cost and price of the Ultrabook will test the appeal of the device, but if consumers can be convinced that the Ultrabook represents the best of both worlds, it will enter the mainstream market. •

Richard Shim is Senior Analyst, Mobile Computing, for DisplaySearch. He can be reached at richard.shim@displaysearch.com.