• The longer the line beam, the greater the potential for dangling bonds and grain-size irregularities, reducing the yield.

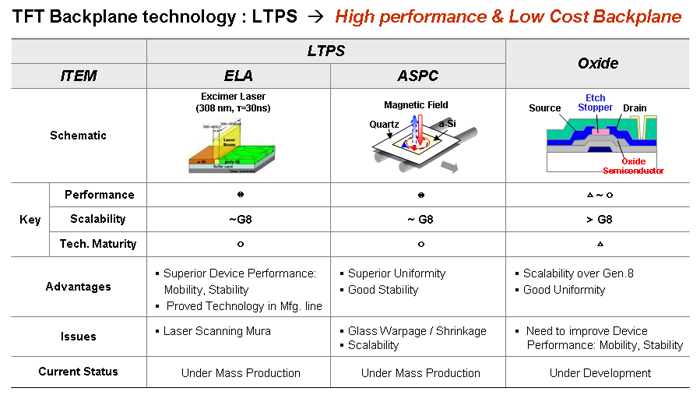

• Alternatives to LTPS using excimer lasers include solid-phase crystallization, which converts a-Si to poly-Si using an annealing process. The operating temperature exceeds 600°C, requiring more expensive glass and causes warping and shrinkage in addition to increasing the component costs and lowering the yields. A second alternative is using multiple metal oxides as the active material. These solutions offer mobilities in the 20 cm2/V-sec range and use the existing a-Si tool sets. However, the technology is immature and does not have the required reliability as yet. Figure 3 compares the three types of backplane solutions.

Fig. 3: TFT-backplane alternatives include excimer-laser annealing (ELA), solid-phase crystalization (SPC), and oxide TFTs.

Frontplane: Vacuum thermal evaporation with a fine-metal mask has been used effectively up to one-half Gen 4 configurations. However, it is believed that this approach has run its course because as the substrate size increases, the weight of the FMM increases and the sag becomes unworkable.

• Alternatives using either polymer or small-molecule material in solution and printing include:

• Ink-jet printing: Epson, Panasonic

• Slot printing: DuPont, Dai Nippon Printing

• Patterning can be eliminated using R,G,B,W with a color filter as proposed by Kodak (but is still needed to form the addressable white subpixels under the color filters).

• Patterning using VTE and laser-induced thermal imaging (LITI) as demonstrated by SMD and 3M.

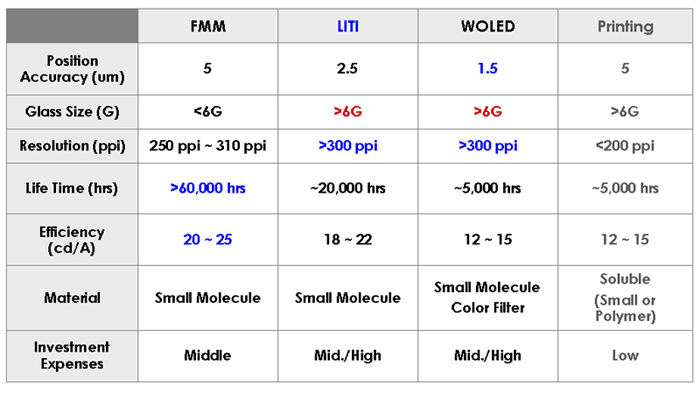

The strengths and weaknesses of the alternatives are shown in Fig. 4.

The existing process of VTE and FMM uses fluorescent and phosphorescent in the native configurations and therefore has the highest lifetimes and efficacies. Each of the other approaches sub-optimizes the material in solution, except in the case of polymers, which are created naturally for solution-based processing. However, the polymers are fluorescent materials and perform less efficiently than phosphorescent materials. In the future, it is likely that if printing or LITI is used, the material will be optimized for that configuration and achieve competitive performance. Figure 4 summarizes the performance and challenges of the alternatives.

Fig. 4: Patterning alternatives for OLED manufacture are compared. Source: Samsung SMD.

Blue Material: The wide band gap in the blue material formulation causes difficulty in getting blue organic material with proper CIE x,y coordinates, efficacy (cd/A), and lifetime. To date, the best material has efficacies of 7–9 cd/A and lifetimes of ~20,000 hours at 1000 cd/m2. What is needed is a blue that has a lifetime > 50,000 hours, an efficacy of ~20 cd/A, and CIE x,y coordinates approaching (0.14, 0.08). Universal Display Corp. (UDC), which has the majority of IP for phosphorescent material (the highest performing organic emitters), offers a unique solution to the problem by proposing a two-blue color approach:

One of the blues is a fully saturated blue, but has low efficacy and low lifetime and would be excited only when a fully saturated blue is required

A second color, sky blue, which has higher efficacy and lifetime, would be excited for all other uses of blue material. The approach would require an added set of subpixel TFTs but would solve the saturated blue problem.

OLED Performance

Much has been written and demonstrated about the front-of-screen benefits of AMOLEDs in terms of

• Black levels

• Viewing angles

• Contrast ratios

• Response time

• Form factor

A discussion of these attributes does not require repetition in this article. However, there are some characteristics that merit some explanation:

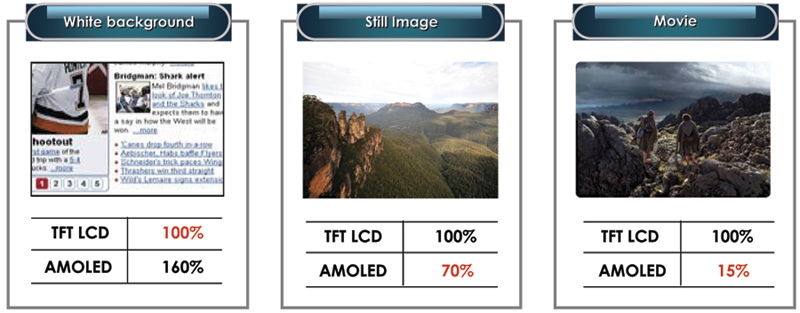

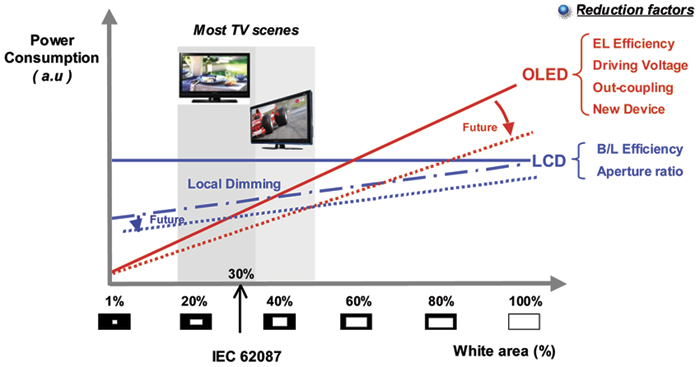

Power Consumption: OLEDs operate at somewhat of a disadvantage vs. most LCDs of the same size when it comes to displaying large-sized all-white areas, but are much more efficient in video and imaging applications, as shown in Fig. 5.

Fig. 5: Power consumption with different backgrounds is compared for TFT-LCDs and AMOLEDs. Source: Samsung SMD.

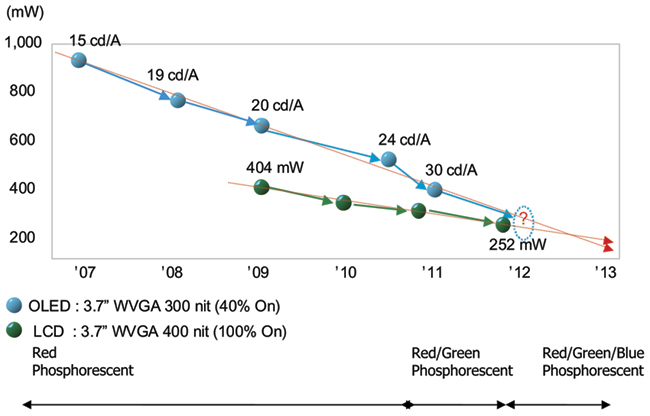

Due to the high percentage of lower gray scales in video and TV applications, AMOLEDs have a natural advantage in power consumption vs. LED TFT-LCDs. This advantage is reduced by 35–50% when rear-lit backlights with local dimming replace edge-lit LEDs, but the share of the rear-lit LED LCDs is less than 1% due to the high price differential. Figure 6 uses actual power consumption on commercial products comparing a 3.7-in. LCD with a 3.7-in. AMOLED. The expanded use of phosphorescent material is expected to result in lower power consumption even as LCDs take advantage of the 10% per annum growth of lm/W forecasted by LED manufacturers. If one translates the trends in power consumption for 3.7 and 40-in. TVs, AMOLEDs could be expected to use 20% less power than rear-lit LED LCDs by 2013, assuming a 40% overall luminance level when displaying real video content, and 40% assuming the normal TV luminance level as shown in Fig. 7.

Fig. 6: AMOLED vs. TFT-LCD power consumption is compared for a 3.7-in. OLED and LCD. Source: Samsung SMD.

Fig. 7: Comparison of LCD- and OLED-TV power consumption. Source: LG Display

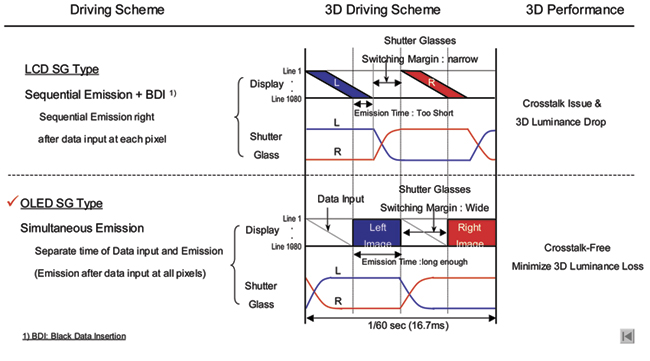

3-D Performance: Yet another benefit of AMOLEDs over TFT-LCDs is the combination of fast response time and 3-D imaging. To realize 3-D, the image is split into two halves: one to address the left eye and the other to address the right eye. The net effect is to halve the time available to resolve the image. Because the LCD operates at a response time of 1–5 msec, it is susceptible to crosstalk, as shown in Fig. 8. However, AMOLEDs, which switch in microseconds, do not suffer from crosstalk and therefore display much sharper 3-D imagery. Plasma TVs also provide a similar benefit, but that response time is not as fast as that for OLEDs.

Fig. 8: A comparison of AMOLED vs. TFT-LCD 3-D performance shows a lack of crosstalk and minimal luminance loss for the OLED type. Source: LG Display.

Short- and Long-Term Degradations: OLED designers must overcome the undesirable phenomena associated with all self-emitting displays – image sticking and differential aging. To prevent image sticking, which could occur on TVs where there are ticker-tape-type images on news and sports programs, the ITO must be pre-treated using plasma to improve the charge stability and reduce the charge redistribution. Differential aging occurs over time when some subpixels are used more frequently than others, and consequently age faster. This issue is overcome by maintaining charge stability and extending the lifetime. Currently, red and green have lifetimes (T50) of greater than 200,000 hours at 1000 cd/m2. Blue has a lifetime of ~18,000 hours at 1000 cd/m2, which translates to 70,000 hours at 500 cd/m2, a typical TV luminance specification. The OLED TVs can meet the lifetime requirements, but a more conservative performance level would be 500,000 to T50.

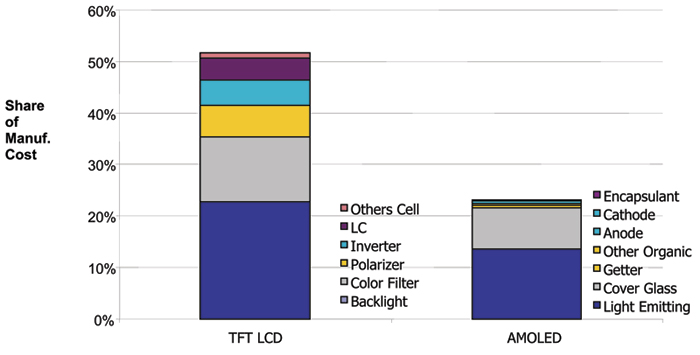

Costs: AMOLED TVs must reach parity with TFT-LCDs in price if they are to attract consumers beyond the early adopter class. LG projects AMOLED TVs to be 3x the cost of TFT-LCDs in 2013, 1.5x the cost in 2015, and 1x the cost in 2017. The cost-down tasks will be to improve the yields from 70% of that of LCDs in 2010 to 100% in 2017, reduce the component costs from 150% of that of TFT-LCDs to 60% by 2017, scale the process from Gen 4 to Gen 8, and reduce the capital costs from 5x that of LCDs to 150% of that of a same-sized LCD fab. Figure 9 is derived from a simulation of AMOLED and LCD 42-in. panel costs on a Gen 8 fab in 2013 and demonstrates that OLED unique-component costs represent only 22% of the total manufacturing costs, while LCD unique-component costs represent over 50% of the total. If AMOLED's other production costs, such as depreciation, labor, overhead, and utilities, are comparable, OLED-TV panels do have an opportunity to be less costly than TFT-LCDs.

Fig. 9: This side-by-side cost comparison for a 42-in. LCD and an AMOLED panel is a simulation based on Gen 8 production in 2013. Source: OLED Association.

In summary, large-area AMOLED TVs may begin to appear as early as mid-2011, but they will be priced at levels that only early adopters can afford. It will not be until the major OLED manufacturers solve the scaling and material issues that AMOLED TVs will be produced for the mass market, which is not likely to occur until 2015. However, if these manufacturers make the right choices in active-matrix backplane technology and in the deposition and patterning of organic material, OLEDs can reach parity in costs with LCDs and the consumer's choice can be driven by performance rather than price.

Flexible OLEDs

Meanwhile, OLED R&D teams are moving forward. Dr. H. K. Chung, advisor to SMD and recipient of the First Annual OLED Leadership award, stated at the OLED Summit in San Francisco in September 2010, that "the next, next big thing is the flexible and transparent OLED, which will result in rollable OLED TVs, the thickness of wall paper." Such a display, as shown in Fig. 10, could be worth the wait. •

Fig. 10: This conceptual image of a rollable AMOLED display could be the TV of the future. Source: Samsung SMD

Barry Young is Managing Director of the OLED Association, www.oled-a.org. He can be reached at barry@oled-a.org.

|

When Can I Get My AMOLED TV?

Prototypes have whetted consumers' appetites for AMOLED TVs. Meanwhile, companies are working to overcome production challenges in order to produce the TVs in volume.

by Barry Young

FLAT-PANEL TVs have taken the TV monitor market by storm, beginning in the early 2000s, and have replaced CRTs as the dominant technology with a 74.4% market share in Q2 '10 (Table 1). Both PDPs, with an 8.0% share, and TFT-LCDs are imperfect solutions, but the consumer has embraced the thin form factor and the larger sizes of flat panels. CRTs were generally limited to < 40 in. on the diagonal, and now flat-panel TVs 55 in. and larger are quite common. However, the anticipated power savings derived from the more-efficient LCDs have been offset by the larger sizes, such that there is a renewed emphasis on reducing power consumption.

Table 1: Q2' 10 TV shipments and shares are shown by technology (RPTV stands for rear-projection TV). Source: DisplaySearch

|

Technology

|

Units (m)

|

Share

|

| LCD TV |

41.8

|

74.4%

|

| PDP TV |

4.5

|

8.0%

|

| OLED TV |

0.0

|

0.0%

|

| CRT TV |

9.9

|

17.6%

|

| RPTV |

0.0

|

0.0%

|

| Total |

56.2

|

100.0%

|

The ascendancy of TFT-LCDs over PDPs is due, in large part, to their flexibility in size and resolution. To achieve full HDTV, plasma TVs need to be at least 40 in. on the diagonal, while TFT-LCD TVs achieve full HD at smaller sizes. Thus, TFT-LCD manufacturers can amortize their investment over a wider product range, including monitors and notebooks, while PDP sales struggle below 40 in. even though it is generally agreed that the plasma colors are more vibrant, the blacks blacker, the contrast higher, the response time faster, and the prices lower than those of LCD TVs. However, it is important to note that in order to narrow these performance differences, TFT-LCD TVs have made significant progress:

• Replacement of CCFLs with LED backlights in approximately 30% of LCD TVs, resulting in thinner form factors, higher color gamut, and lower power consumption.

• Edge-lit LED technology that can reduce the thickness of LCD TVs to < 15 mm.

•Rear-lit LED LCDs with local dimming; a 50% improvement in power consumption also comes with a dynamic contrast ratio benefit.

• Color filters and polarizers that are more efficient and less expensive to produce.

Advent of OLEDs

Recently, OLED-display manufacturers have recognized both 2-D and 3-D TVs as a new opportunity. The first OLED TV, 11 in. on the diagonal with a 3-mm-thick panel, was introduced in late 2007 by Sony; the second, a 15-in. HD TV that was 2.7 mm thick, was introduced in late 2009 by LG Display. Neither of these TVs demonstrated the scalability or the financial viability of the process. However, they did show that the consumer recognized the performance differential and could visually observe the front-of-screen benefits of OLEDs. The new TVs set off a wave of speculation as to when OLED TVs would be introduced at larger sizes with competitive prices. What these speculators did not take into account was that both TVs had been produced on Gen 3 fabs and at low volumes, so the costs were extraordinary, as reflected in prices of approximately $2500. But OLED manufacturers have continued to perfect their technology, and at the 2010 IFA show in Berlin, LG recently showed a 31-in. 2.7-m-thick full-HD AMOLED TV with the capability to handle both 2-D and 3-D (Fig. 1.)

Fig. 1: LG recently introduced a 31-in. 27-mm-thick full-HD AMOLED TV at a trade show in Berlin. Image courtesy LG Display.

Concurrent with the release of the three TV demonstration products from Sony and LG, Samsung Mobile Display (SMD) began mass producing millions of AMOLED smartphone displays on a Gen 4 (730 mm x 920 mm) fab. And while doing so, the company solved many of the production-level challenges of AMOLEDs, including:

• Full color patterning using vacuum thermal evaporation (VTE) and fine-metal masks (FMM).

• TFT production using low-temperature polysilicon (LTPS) for smartphone displays with yields greater than 80% with sufficient reliability and uniformity

• Integration of phosphorescent red with fluorescent green and blue.

• Microcavities and top emission

• Pixel densities exceeding 250 ppi

• Power consumption with 40% of the pixels on at comparable levels to that of TFT-LCDs

• Production costs, even absorbing depreciation close to Gen 4 LTPS-LCD fabs.

Recently, Samsung (SMD) announced that it was building a Gen 5.5 fab (1300 x 1500 mm) that would be ready for mass production in 2011, and it is likely that LG Display will follow closely behind. Because Gen 5.5 has the capacity to produce six-up 31-in. panels and LG demonstrated a 31-in. OLED TV, the announcement was taken by many people as a sign that the new fabs would be used for OLED TVs. However, instead, Samsung has reported that it expects to use its capacity for small-to-medium–sized displays to fulfill the extraordinary demand for AMOLED panels used in smartphones.

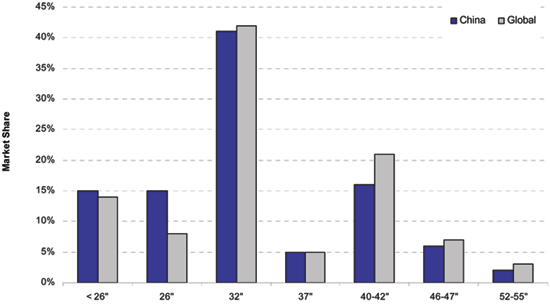

Therefore, a small volume of 28-, 31-, and 40-in. TV panels can be expected in the near future, but both SMD and LG Display agree that the output of a Gen 5.5 will not be price-competitive with TFT-LCDs built on Gen 6, 7, and 8 fabs. Table 2 compares the number of panels per substrate for each of the fabs. Although Gen 5.5 can fit six-up 31-in. panels, Gen 8 will produce 18 panels and the per panel costs of labor, depreciation, and overhead will be lower for Gen 8 than for Gen 5.5. As shown in Fig. 2, the market for 31-in. and smaller-sized LCD TVs is 70% of the total, but this area is very cost-sensitive and not the best opportunity for higher-end consumers.

Table 2: Panelization for Gens 3, 4, 5.5, 6, and 8 are compared above. (W stands for wide form factor.) Source: DisplaySearch

| Generation |

Size

|

W28

|

W31

|

W37

|

W40

|

W42

|

W46

|

W47

|

W52

|

W55

|

| Gen 4 |

730 x 920

|

2

|

2

|

1

|

1

|

0

|

0

|

0

|

0

|

0

|

| Gen 5.5 |

1300 x 1500

|

6

|

6

|

3

|

2

|

2

|

2

|

2

|

2

|

2

|

| Gen 6 |

1500 x 1850

|

10

|

8

|

6

|

4

|

3

|

3

|

3

|

2

|

2

|

| Gen 7 |

1870 x 2200

|

15

|

12

|

8

|

8

|

6

|

6

|

6

|

3

|

3

|

| Gen 8 |

2200 x 2500

|

18

|

18

|

10

|

8

|

8

|

8

|

8

|

6

|

6

|

Fig. 2: A distribution of LCD TVs by size for Q2 '10 shows the largest market share by far belongs to the 32-in.-diagonal products. Note: "Global" legend at top excludes China.Source: Wits View.

Given the plans for Gen 5.5 by SMD and LG, it can be assumed that the manufacturing process will scale beyond 730 mm x 920 mm. In fact, SMD will likely use the same technology for Gen 5.5 as it is using for Gen 4.5 by cleverly partitioning the manufacturing process. For example, by increasing the excimer-laser line beam to longer than 420 mm, two excimer lasers can be used to concurrently convert a-Si into poly-Si on a Gen 5.5. Moreover, a Gen 4 vacuum thermal evaporation (VTE) tool can be used to deposit and pattern the organic material using shadow masks, even if the substrate is held horizontally. One short-term innovation is the use of a linear array where the substrate is held vertically to double material utilization, minimize the fine-metal mask (FFM) sagging, and eventually allow a larger size substrate.

Technology Challenges

However, these innovations will not solve the cost challenges for AMOLED TVs. Dr. S. S. Kim, CTO of Samsung Mobile Display, claimed at SID's Display Week in May 2010 that AMOLED TVs were "the next big thing," but that it would take a Gen 8 or larger fab to achieve cost parity with LCDs. There are several technology challenges that need to be overcome in order for AMOLEDs TV panels to be built on Gen 8 substrates:

Backplane: Although LTPS has proven to be a mature solution for backplanes up to Gen 5.5, LTPS creates substantial problems to scale to Gen 8:

• LTPS has very slow total average cycle time (TACT), more than double the typical 60 sec for a-Si, and the capital cost for the array process is twice that of a-Si.

• Scaling up the excimer line beam typically increases the non-uniformity, which at a minimum complicates the compensation circuitry.

|