New Trends in Touch

New Trends in Touch

With touch panels becoming ubiquitous, the touch industry is undergoing rapid change. Touch Display Research, Inc., reports on its most recent survey of the leading manufacturers in the touch-screen, ITO-replacement, and touchless-control industries.

by Jennifer Colegrove

THE touch-panel market has grown

explosively since 2006. As the first industry analyst to write a comprehensive touch-screen industry report in that year, I feel very fortunate to have witnessed touch-screen engineers, technicians, and managers grow the industry through hard work and constant innovation. Despite a global economic recession over the last couple of years, the market has continued to expand at a handsome rate.

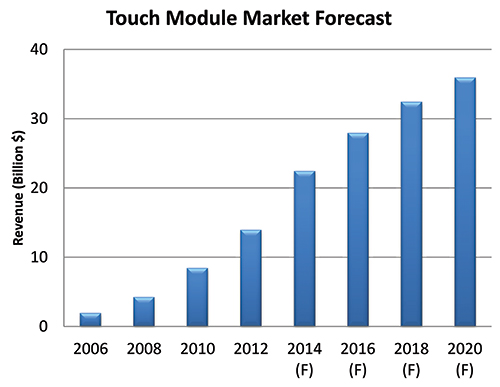

As shown in Fig. 1, Touch Display Research forecasts1 that touch-module revenue will reach $36 billion by 2020, up from just $2 billion in 2006.

Touch-screen suppliers, especially projected- capacitive-touch suppliers, were mostly profitable during 2007 and 2009. But fast forwarding to 2014, the competition is fierce, with many touch-screen suppliers now encountering net losses. New business strategies are needed for companies to become leaders or maintain

leadership positions in today’s touch industry.

Fig. 1: The touch-module market forecast calls for rapid advances through at least 2020. Source: Touch Display Research, Inc., 2014.

ITO Replacement: Non-ITO Transparent Conductors

ITO is still the mainstream transparent conductor used for touch panels; however, due to ITO’s high cost, fragility, and long process steps, ITO replacements have become one of the hottest trends. There are currently more than 10 types of ITO replacement technologies. I have placed them into six categories: metal mesh, silver nanowire, carbon nanotube, conductive polymer, graphene, and other transparent

conductor technologies. In addition, there are over 200 companies or research institutes that are currently working on ITO replacements.2

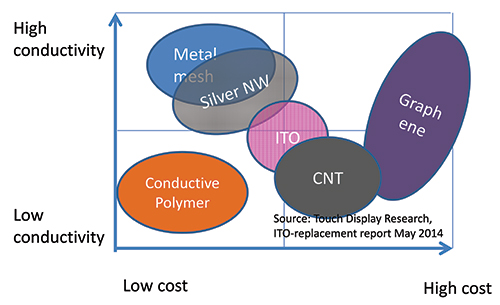

Each technology has its pros and cons. There are many characteristics to compare when choosing a transparent conductive material – sheet resistance, transmissivity, conductivity, haze, optical appearance, and cost are just several examples. Figure 2 compares cost and conductivity.

Fig. 2: ITO replacements are compared in terms of cost vs. conductivity. Source: Touch Display Research, ITO replacement: non-ITO transparent conductor technologies, supply chain and market forecast report, 2013 and 2014.

In late 2012 and early 2013, the shortage of touch screens for notebooks, ultrabooks, and all-in-one PCs – due to the high demand of touch from Windows 8 devices, coupled with a low yield of 10–29-in. ITO touch sensors – drove the adoption of ITO replacements.

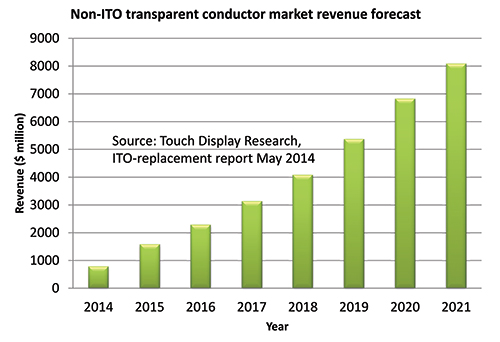

After many touch-panel suppliers ramped-up capacity in mid-2013, the shortage turned into an oversupply by the end of that year, which resulted in substantial touch-screen-module price erosion. Touch Display Research expects the average selling price (ASP) of touch modules to continue to fall below $40 for notebook PC sizes, which, in turn, will expand the opportunities for low-cost ITO replacement. As a result, the non-ITO transparent-conductor market revenue is forecasted to increase from $798 million in 2014 to $8.1 billion in 2021 (Fig. 3). (Note: Not all ITO replacements are low-cost alternatives; some, such as graphene, are still more expensive than ITO.)

Fig. 3: The non-ITO transparent-conductor market is forecasted to reach $8.1 billion in 2021. Source: Touch Display Research, ITO-replacement: non-ITO transparent conductor technologies, supply chain and market forecast report, May 2014.

Active-Pen Technologies

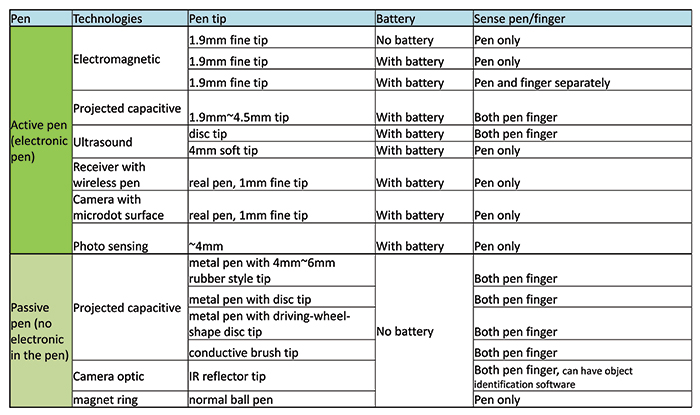

While finger touch is intuitive, active-pen writing is accurate, easier, and can add a personal touch. Pen input is very useful in education and in certain types of language input, as well as in medical, financial, industrial, and content creation or markup applications. Touch Display Research defines an active pen as one with an electronic circuit. Some active pens have an integrated battery in them, some not. A passive pen has neither an electronic circuit nor a battery. According to our research, there are nine types of active-pen technologies and six passive-pen technologies, as summarized in Fig. 4.

Fig. 4: Active pens and passive pens are compared in terms of technologies, pen tips, batteries, and sensing interfaces. Source: Touch Display Research, Active pen technologies, supply chain and market forecast 2014 report.

In 2007, when Apple released the first iPhone with a projected-capacitive touch screen, it had the benefit of multi-touch, zero-force touch, good durability, etc. Referring to the first iPhone at the Macworld Expo in 2007, Steve Jobs told his audience, “Nobody wants a stylus. So let’s not use a stylus. We’re going to use the best pointing device in the world. We’re going to use a pointing device that we’re all born with – born with 10 of them. We’re going to use our fingers.”3 Job’s point of reference for this statement was the old resistive touch pen. Since 2011, Apple has been investing heavily in active pens, and it’s my strong belief that Apple will release an active pen soon.

Samsung’s Galaxy Note series has successfully adopted active pens since 2010. The company’s active pen is an electromagnetic type made by Wacom.4 N-trig’s active-pen and sensor technology has been adopted by over 10 touch-screen device models.5 In addition, many active-pen companies have raised funds on Kickstarter. Over 10,000 individuals have backed those pen projects.6

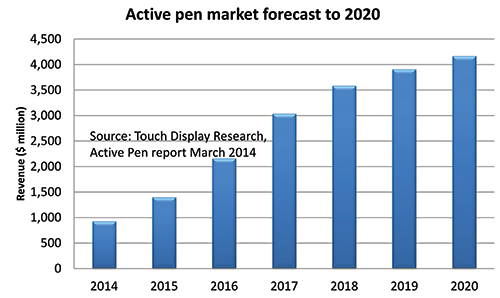

Active-pen technology is superior to passive-pen technology in terms of accuracy, pressure sensing, and ability to draw fine lines. Active-pen usage should therefore experience rapid growth in the next several years. Touch Display Research forecasts that the market for active-pen writing modules (including pen sensor, one pen, and the controller IC) will increase from $931 million in 2014 to $4.17 billion in 2020 (Fig. 5).

Fig. 5: The active-pen writing-module market will increase significantly over the next 7 years. Source: Touch Display Research, Active pen technologies, supply chain and market forecast 2014 report.

Touchless Control

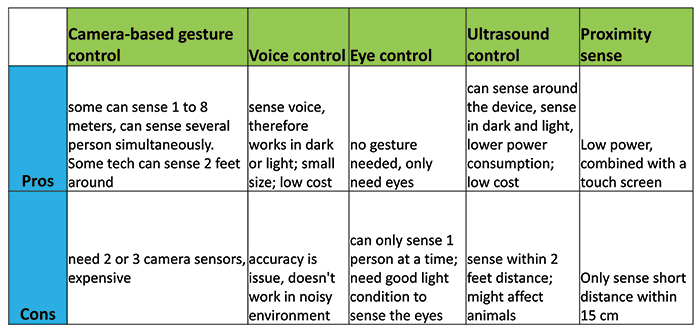

While touch screens are ubiquitous, touchless control is also expanding. Touchless control has the benefit of being clean (no fingerprints) and hygienic (no germs). It also has the potential to be easier and more fun, depending on the application. Touchless control does have its downside, as shown in Fig. 6.

Fig. 6: Touchless control technologies include camera-based gestures, voice, eye, ultrasound, and proximity. Some of the pros and cons of each interface are compared above. Source: Touch Display Research, Touch and Emerging Display Monthly Report, 2014.

Here are some of the types of touchless control, along with their benefits and drawbacks.

Camera-based gesture control: The most popular example is Microsoft’s Kinect, which uses PrimeSense’s camera-based optical sensing technology. Gesturetek also provides camera-based sensing technologies.

Eye control: Eye control, also known as eye tracking, has increased in popularity in recent years. In fact, the technology has been around since the 1900s (using film cameras). Since the 1970s, video cameras replaced film cameras for eye control. At that time, most applications were medical (helping disabled individuals), or research driven, and, as a result, prices were very high. Since 2000, driven by consumer demand, camera (image sensor) prices have declined significantly. As a result, eye control has become more affordable.

Voice control: Voice control is now used in automobiles and mobile phones. Microsoft released voice-control software for mobile phones in 2003, but it was not popularized until Apple adopted Siri on the iPhone in 2011. In 2013, Intel mandated that voice control be facilitated on all Intel-based ultrabooks.

Ultrasound control: This technology can sense not only in front of devices but around them, and in both dark and light ambient situations. Some industry experts have indicated that ultrasound might in some way adversely affect animals.

Proximity sense: This is short-distance sensing, typically up to 15 cm from a touch-screen surface. Proximity sensing is typically combined with projected-capacitive touch screens, camera-based optical imaging, or infrared touch screens. Compared to camera-based gesture control, proximity sensing exhibits lower power consumption, roughly 10% that of camera-based systems.

Business-Strategy Recommendations

With the touch-screen-module market forecasted to grow to $36 billion by 2020 from just $2 billion in 2006, there will be many new opportunities in the fast-changing touch industry. In addition, the shortage and subsequent oversupply of ITO touch sensors created opportunities for ITO replacements, of which there are many, as described earlier in this article. The global non-ITO transparent conductor market is forecasted to grow to $8.1 billion by 2021, from $798 million in 2014.

Touch Display Research recommends metal mesh for simple designs with large volumes; silver nanowire for display and OLED lighting applications; conductive polymer for EMI and anti-static applications (due to low conductivity and prices); and carbon nanotube or Canatu’s Carbon NanoBuds for mobile/wearable devices because of this technology’s flexibility, low reflection, and near-zero haze. These last two qualities are essential for sunlight readability, and mobile/wearable devices are likely to be used in sunlight rather frequently.

In addition, companies that take strategic advantage of any of the other touch-related trends mentioned above have a better chance of succeeding over the long run. Pen and finger simultaneous touch are the ideal human–machine user interface for education, industry, and certain language usage. Active pens are obviously a growth area. And touchless control is expanding; it will have good penetration in TV, medical, public signage, and gaming applications.

References

1“Touch and Emerging Display,” Touch Display Research, Inc., Monthly Report.

2“ITO replacement: non-ITO transparent conductor technologies, supply chain and market forecast” report, Touch Display Research, Inc., Monthly Report, May 2014.

3https://www.youtube.com/watch?v=P-a_R6ewrmM

4“Wacom’s feel technologies bring enhanced responsiveness, productivity, and efficiency to Samsung’s Galaxy NotePRO,” Feb 12, 2014; www.wacom.com/en/us/overlays/articles/2014/us-1030

5www.n-trig.com

6“Active pen technologies, supply chain and market forecast” report, Touch Display Research, Inc., Monthly Report, March 2014. •

Jennifer K. Colegrove is the founder, CEO, and analyst of Touch Display Research, Inc. She writes reports and performs consulting projects focusing on touch and display technologies, including touch screens, ITO replacement, active pen, near-to-eye displays, flexible displays, OLED displays and lighting, 3-D displays, e-paper displays, pocket projectors, gesture control, voice control, and eye control. She can be reached at jc@TouchDisplayResearch.com or 408/341-5065.