Plastic Displays Will Play a Major Role in Automotive HMIs

Plastic Displays Will Play a Major Role in Automotive HMIs

Plastic Displays Will Play a Major Role in Automotive HMIs

Automotive trends, including increasing reliance on the human-machine interface (HMI) for the vehicle, indicate that future displays will need to be curved and shaped to fit any surface in the car. To speed adoption and reduce costs, it is desirable that this new generation of displays is manufactured using the existing automotive supply chain and building as much as possible on proven technologies.

by Simon Jones

THE automotive industry is on the threshold of several parallel disruptive changes driven by technology advancements and business model evolutions. For example, the combination of increasingly autonomous vehicles and new shared-ownership models is expected to lead to a much greater number of passenger miles being traveled without a pro rata increase in vehicles on the road.1

These changes will impact the driving experience as supported by the human machine interface (HMI) of the car. This is already happening as vehicles become more connected and more automated on their way to being driverless. Displays and touchscreens will represent a major platform for the new HMI, and flexible, conformable, plastic displays will help meet safety and usability needs while also enabling manufacturing and cost efficiencies.

Safety, Efficiency, Usability

HMI innovations that address both safety and usability will incorporate multiple sensors and cameras around the car that, if well integrated with the HMI, can warn of hazards on the road. A compelling example is the transparent A pillar concept in which the pillars on either side of the windshield are equipped with conformable wrap-around displays. Cameras on the outside of the car capture images that are then projected onto the display to make the A pillar seem transparent, as illustrated in Fig. 1. This will allow the driver to respond more intuitively to the hazard than if the warning came from the instrument panel or the center stack display.

Fig. 1: The transparent pillar concept is illustrated here. The supporting pillar on the left next to the windshield appears transparent to the driver, revealing potential road hazards. This is enabled by a conformed wrap-around display that is projecting an image from an external camera. Image: FlexEnable

In addition to the safety benefits, conformed and shaped displays can also contribute to increased fuel efficiency by allowing the removal of the outside side-view mirror, which the Auto Alliance estimates can reduce drag by up to 7%.2 The obvious and natural location for the mirror replacement display is on the A pillar on the inside of the cabin.

Another driver for increased use of displays is the very strong preference of users. According to research conducted by IHS Markit, users prefer touchscreens over all other forms of input.4 In contrast, physical buttons tend to be the least popular input device, so it is no surprise that buttons are fast disappearing in favor of touch displays.

As vehicles become more autonomous over time, needing less and less intervention from drivers, users may be seated in different areas of the vehicle, where they can perform a variety of tasks other than driving (Fig. 2). If surfaces within the car have been made active through the integration of conformed and shaped displays, then it becomes possible for the HMI to move around with the user to provide connectivity and entertainment wherever the user happens to be.

A more near-term trend in automotive displays is that the instrument panel and center stack displays are rapidly getting larger. However, it is becoming increasingly difficult to accommodate large and flat displays in an ergonomically optimized interior design where every other surface is curved.

Fig. 2: The XiM17 interior concept from Yanfeng Automotive Interiors demonstrates several potential uses of curved displays, including a door-panel display and a floor-console display.3 Yanfeng is actively sourcing conformable display technologies from a number of sources to make this concept a reality. Image: Yanfeng Automotive Interiors

A Significant Opportunity for Automotive Display Makers and Tier 1s

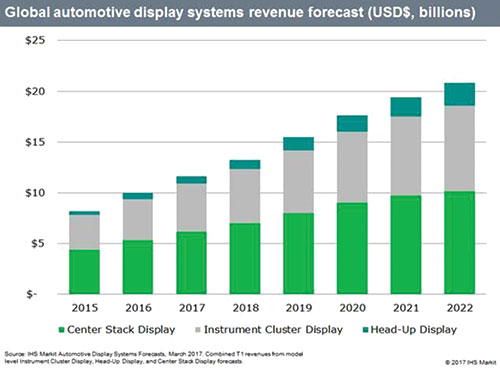

A trend toward rapidly increasing unit volumes and larger sizes of displays in vehicles is already clear. According to IHS Markit, growth for head-up, instrument cluster, and center stack displays is projected to rise through at least 2022 (Fig. 3). IHS Markit also predicts a growth hot spot in 7-in. to 8-in. displays for the center stack and instrument cluster, which will alone account for more than 50 million units in 2020. FlexEnable projects that A pillar displays, steering wheel displays, entertainment displays, and many other new display applications in the car will represent significant upside opportunities to these forecasts.

Fig. 3: Growth for head-up, instrument cluster, and center stack displays is projected to rise steadily through 2022 and beyond.4 Image: IHS Markit

The longer-term advent of self-driving cars does not negate this trend for two reasons. First, the industry expects that partially self-driving cars will be prevalent for a long time before we have cars that can self-drive in all circumstances. This means that the HMI has the additional task of managing the handover of responsibility between the car and the driver, with obvious safety implications. Second, even a fully self-driving car will have an extensive HMI to address the entertainment, information, and communication needs of the passengers. This underscores the desirability of using the curved surfaces of the interior to implement an extensive, seamless, and customizable HMI.

Non-flat and non-rectangular displays present new system integration challenges. The displays will typically be manufactured in a flat state and will then need to be formed into the shape that is required for the final vehicle design. This will typically require lamination and assembly into a shaped cover glass or “window.” The design of the window is likely to be highly customized to the vehicle interior design. This creates an opportunity for Tier 1s to add more value at the display module level, working closely with display makers and vehicle manufacturers. In many cases, the HMI features enabled by the conformed display will also require the Tier 1 to design and deliver a system that may include cameras and significant image processing. All of this means that there is more at stake in the supply chain and more value creation opportunity than is represented by the display module alone.

The challenge for the supply chain is clear. It needs to deliver conformed and shaped displays that meet the automotive industry’s tough environmental standards at reasonable cost, and at a pace that matches accelerating innovation in vehicle design and use.

Flexible OLED vs. Flexible LCD

OLED and LCD are the two leading candidates for conformed and shaped displays in cars, and both present manufacturing challenges in that special techniques and methods are needed to be able to make the display on a flexible plastic substrate.

Flexible OLED is typically made by coating polyimide on a glass carrier. The OLED stack is then fabricated on the substrate using conventional high-temperature processes and later separated from the glass using a laser release method. A key challenge of this methodology is the relatively low yield of the laser release process, which typically destroys the

glass carrier. After fabrication, another challenge is meeting the demanding reliability and lifetime requirements of automotive applications. OLEDs are highly susceptible to contamination from moisture and oxygen, driving the need for an extremely high-performance, flexible-barrier-layer solution. Automotive applications are particularly challenging because the range of temperature and humidity conditions are much wider than for consumer devices, and the display is required to last for at least 10 years. In addition, automotive OEMs are

currently specifying a luminance of up to 1,000 cd/m2 and may require even brighter displays in the future. These very high levels of luminance may be impossible to achieve with OLED while simultaneously achieving the required lifetime.

The key challenge with LCD-based panels is that they require the substrate to be optically very clear. Substrates that can survive high-temperature processes and maintain optical clarity and non-birefringence exist but are very expensive. However, the industry already has extensive experience in how to engineer LCDs to work in vehicles, and an automotive-qualified supply chain for LCDs already exists. The high-luminance requirement can be met with a high-performance backlight without limiting the lifetime of the display, whereas with an OLED display, increased luminance will directly reduce its lifetime.

Figure 4 shows a flexible, plastic organic LCD (OLCD) that has been developed by the author’s company.

Fig. 4: FlexEnable’s plastic organic LCD (OLCD) is shown here in a cylinder form factor. OLCD displays can be curved to bend radii of below 30 mm.

Low-temperature Processes and Commodity Substrates Enable Cost-effective, Flexible LCD

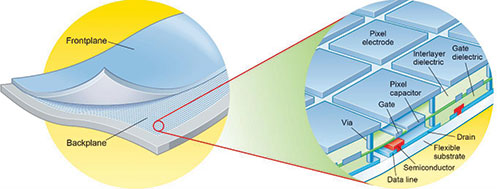

An alternative to sourcing expensive, high-temperature substrates is to use low-temperature processes to enable the use of commodity substrates. This is particularly critical for the fabrication of the active-matrix TFT array, which conventionally relies on high-temperature vacuum deposition of semiconductors and dielectrics. The author’s company has developed an industrial process for fabricating the active matrix at low temperatures in air using solution-coated organic materials (Fig. 5).

Fig. 5: Plastic active-matrix backplanes can be applied to a number of frontplane technologies, including electrophoretic, LCD, and OLED.

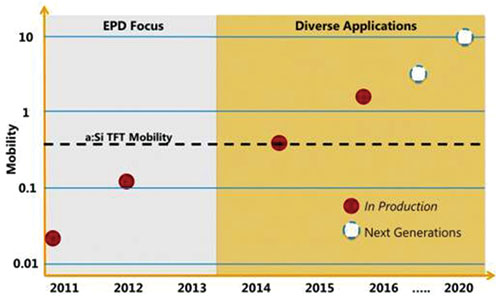

Organic TFT (OTFT) technology is already in commercial production for flexible electrophoretic displays by Plastic Logic GmbH and this same technology platform has now been adapted to flexible organic LCDs (OLCDs) by FlexEnable. This adaptation has been made possible by rapid progress in the performance of OTFTs, which now exceed conventional amorphous silicon TFTs in mobility (Fig. 6) and stability, as has been described, for example, in the paper, “Photolithographic Integration of High Performance Polymer Thin-Film Transistors,” presented at Display Week 2016 by Merck.5

Fig. 6: The mobility of production OTFT processes now exceeds the performance of amorphous silicon.

This low-temperature process allows the use of triacetylcellulose (TAC) film as the substrate, which is already used as the substrate for LCD polarizers. This opens the prospect of using the same substrate for the polarizer and the active-matrix backplane for ultimate thinness.

OTFTs manufactured with this process are also fundamentally stable, as indicated by gate bias stress tests (see Table 1). As the semiconductor is p-type, the key parameter is positive gate bias stress (PGBS). The PGBS test is conducted by applying a constant bias voltage to the TFT for a fixed amount of time. The switching characteristics of the OTFTs are tested before and after the fixed stress. The results indicate that there is only a 1V shift in the switch-on voltage of the OTFT, which is half the shift seen in amorphous silicon devices.

Table 1: Table 1: Gate Bias Stress Test Results

| TFT Technology |

Test |

Voltage |

Temperature |

Time |

|ΔVth| |

| Organic |

Positive Gate Bias Stress (PGBS) |

+20V |

60°C |

10,000 sec |

1V |

| Amorphous Silicon6 |

Negative Gate Bias Stress (NGBS) |

–20V |

60°C |

10,000 sec |

2V |

Of course, the automotive industry requires qualification over an extensive set of environmental parameters. This work is under way for OLCD, and FlexEnable’s 14-in. prototype line is running at up to three shifts per day to produce the prototypes and test samples necessary. Working with manufacturing partners, FlexEnable is already in the early stages of scaling OLCD to volume production. Final automotive qualification of production OLCD modules is targeted to start in 2018.

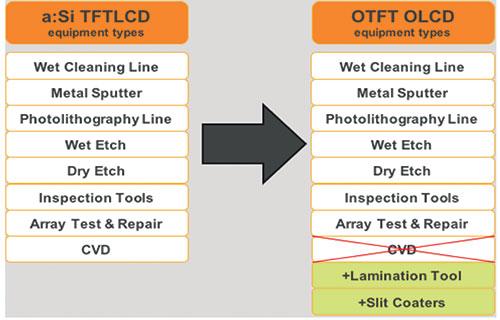

Re-purposing Existing Fabs to OLCD

The OLCD process has been developed to minimize the investment required to convert an existing amorphous-silicon-on-glass TFT fab to OTFT. Often, a fab can be reconfigured to make OTFT samples with no capital investment at all, although to create a fully balanced fab will require some additional coating and lamination machines. This is a very modest investment compared with the original capital investment required to build the fab.

The process begins by laminating the low-cost plastic substrate to a carrier glass. The OTFTs are then fabricated on the substrate before the LCD frontplane is created using largely conventional (and therefore low-cost) materials and processes.

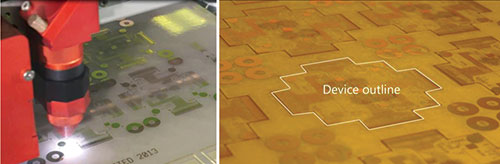

A simple process is used to de-mount the finished displays from the glass carrier at extremely high yield and allows the glass carrier to be re-used. Before individual displays are de-mounted from the carrier glass, they can be laser cut using a commodity CO2 laser trimming tool to almost any arbitrary shape. In the example shown in Fig. 7, a laser is being used to cut out a non-rectangular test sample.

Fig. 7: Cutting OTFTs to arbitrary shapes is done with a standard CO2 laser trimming tool. The left-hand picture shows the laser cutting tool cutting the non-square outline of the fabricated device shown in the right-hand picture. The cutting process takes place while the plastic device is mounted on the glass carrier for processing. The device is de-mounted using a low-stress heat-based de-mount process.

The ability to re-purpose existing active-matrix LCD fabs to make OLCDs, together with process simplifications and efficiencies that result from using a low-temperature process, means that the OLCD is an extremely cost-competitive approach to making plastic conformable displays. Cost modeling based on analysis of specific partner fabs indicates that flexible LCD can reach the cost of standard glass-based LCD at scale, which means that flexible OLCD will maintain a significant cost advantage over flexible OLED even when the latter process is fully scaled.

Today’s LCDs for automotive applications are typically manufactured on Gen 4.5 lines (730 mm by 920 mm). The tool set typically used is listed in Fig. 8.

Fig. 8: A fully balanced line conversion for OLCD will typically require some additional lamination and coating tools.

When a line is re-purposed to make plastic OLCD panels, the chemical vapor deposition tools are replaced with solution deposition tools such as slot-die coaters. Also, laminators would typically be added to mount the low-cost plastic substrate to the glass carrier for processing. After these modifications to the fab are made, the manufacturing process for the OLCD is very similar to a glass LCD. The OTFT array and color filter array are made on separate sheets and assembled together on a one-drop fill line with photospacers added to define the cell

gap. Significantly, no special equipment is needed to de-mount the plastic from the glass because the low-stress heat-based de-mount process is an exceptionally elegant step that protects the integrity of cell gap when the glass carrier is removed.

OLCDs are driven in the same way as are glass-based displays. Row and column drivers are bonded to the array substrate using standard interconnect technologies like chip on film (COF) or chip on glass (COG), which have been adapted for processing on plastic. Row drivers can be integrated on the OTFT array substrate for certain display designs.

HMI Innovation Is Enabled by Conformed and Shaped Displays

One of the great advantages of re-purposing the existing automotive LCD supply chain is that time-to-market can be minimized as well as the cost and risk of adoption. Already, visionary manufacturers are implementing radically new HMI features with prototype conformed and shaped displays.

Looking further into the future, we can imagine a car interior where there is a “hidden until lit” touchscreen almost everywhere there is a physical button today. Every aspect of the HMI would then become highly personalizable, upgradable, and reconfigurable, according to the application being used. Personal customization of the HMI, and even the ambience of the interior, will become possible, and this will be increasingly important as “shared mobility” models lead to each car being used by more people on average.

In order to realize the applications described in this article, major car brands are working toward product introductions starting in 2019, enabled by supply-chain-friendly technologies like OLCD. The car interior of the near future is going to look very different, very soon.

References

11KPMG: “The Clockspeed Dilemma,” https://assets.kpmg.com/content/dam/kpmg/pdf/2016/02/us-jnet-auto-clockspeeddilemma.pdf

2www.wired.com/2014/04/tesla-auto-alliancemirrors

3Yanfeng Automotive Interiors: “XiM17:“The Next Living Space Interior Autonomous Concept Car Debuts at NAIAS 2017,” www.youtube.com/watch?v=56Ow8cw1m6o

4IHS Markit: “2017 IHS Markit Connected Services and Apps Consumer Survey.”

5S. Bain, P. Miskiewicz, I. Afonina, and T. Backlund, “Photolithographic Integration of High Performance Polymer Thin-Film Transistors,” SID Symposium Digest of Technical Papers 47, No. 1, (2016).

6M. J. Powell et al., Journal of Non-Crystalline Solids, 137 and 138, 1215–1220 (1991). •

Simon Jones is commercial director at FlexEnable and has been developing applications of flexible electronics for more than 10 years. He has a particular focus on forming the supply chain partnerships needed to ensure the successful commercialization of organic and flexible electronics over a range of applications and manufacturing scenarios. He can be reached at simon.jones@flexenable.com.