How LEDs Have Changed the LCD Industry

LED backlighting has attracted a great deal of interest from the LCD industry over the last few years. The introduction of LED backlighting was not just a simple change to the panel structure; it affected the LCD industry in many ways, including product trends, economics, business strategies, and supply chains.

by Jimmy Kim and Paul Semenza

BEFORE THE BOOM of light-emitting-diode (LED) backlighting in the 2008–2009 time frame, TV makers used LEDs primarily to enhance the color gamut and contrast ratio of their products. This led to an increase in material costs, but makers expected the enhanced picture quality to add much more value to their products. However, they discovered that consumers were unwilling to pay a lot more money for picture quality. The penetration of LED backlighting did not increase, and most LCD TVs continued to use cold-cathode fluorescent lamps (CCFLs).

Eventually, the focus of LED backlighting for TV products shifted from picture quality to design. Makers focused on slim LED edge-backlit TVs. These were still more expensive than conventional CCFL-backlit TVs, but the price gap decreased significantly with the introduction of edge backlighting. Consumers were willing to pay more for design than for picture quality, and the penetration of LED backlighting started to increase.

What is the difference between these two cases? Picture quality is often thought of as a relative feature, valid only when compared to other products. Design is an absolute feature – no comparison is needed to see it. It seems that consumers will pay for an absolute benefit – LED backlighting showed that design can be a strong marketing tool in the TV market place. This trend toward design continues. At CES 2012, many companies exhibited narrow-bezel TVs and ultrabook models.

Value Creation for LCD Makers

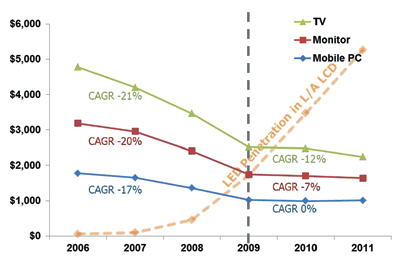

LED backlighting allowed panel and set makers to add more value to their products and lower the rate at which panel and set prices were dropping. By comparing LCD panel-area prices with LED penetration into large-area-LCD panel shipments (Fig. 1), it can be seen that panel prices stabilized after the 2009 boom in LED edge-backlit TVs. TV makers began filling their product lines with LED-backlit models after that time. The intention was to increase, or at the least maintain, total revenue in the event that prices continued to drop sharply in the display industry.

Fig. 1: LCD panel prices fell rapidly until 2009, when LED penetration began to increase. Source: DisplaySearch, Quarterly Worldwide FPD Shipment and Forecast Report and Quarterly Large-Area TFT LCD Shipment Report. (Note: CAGR is the Compound Annual Growth Rate).

Revolution in the LCD Business Model

A more fundamental change resulting from the LED-backlighting boom in the LCD industry relates to the structure of the supply chain. The clearest example of this is the emerging open-cell business model (in which LCD makers ship panels without backlights), which is shifting value in the LCD supply chain from panel makers to set makers and has been accelerated by the introduction of LED backlighting.

The origin of the open-cell business model dates back to 2005. As shipments of large-sized LCD TVs increased, the cost of the large numbers of CCFL tubes and inverters became a concern. With increasing panel size and resolution, as well as the introduction of 120/240-Hz frame rates, the luminance requirement for backlighting increased. This made decreasing the number of CCFLs even more difficult, so panel and set makers focused on reducing the costs related to inverters.

Some set makers focused on the overlap of power components in TV sets and LCD modules. The switching-mode power supply (SMPS) in a TV set provides 24 V DC from a 100 to 240 V AC current supply. The inverter in the LCD module converts the 24 V DC back to AC current at more than 1000 V. This duplication can be eliminated by combining the inverter and SMPS into one power board, the so-called integrated power board (IP board), saving cost and increasing efficiency.

The IP board became part of the power supply of the TV set, so set makers could use LCD modules without inverters, which meant that the value of the backlighting started to shift from panel makers to set makers. However, IP boards did not lead to broad use of the open-cell model; only a few Taiwanese makers supplied open cells to set makers. Set makers did not want to expand the IP board business to an open-cell business entirely, and only accepted IP boards for a limited number of models.

The adoption of LEDs in backlights simplified the electrical circuitry, and the open-cell business began to accelerate after the increase of LED penetration in 2009. Many panel makers increased shipments of open cells. According to DisplaySearch's research, open cells accounted for 25% of LCD-TV panel shipments in 2011, and the share will nearly double in 2012.

What Happened after 2009?

For set makers, lack of expertise in CCFLs was the main obstacle to moving more quickly to the open-cell model. CCFLs contain mercury, which makes them hard to control under even slight temperature changes. Set makers were not as experienced in dealing with CCFLs as panel makers and they faced quality issues if they used open-cell panels. LEDs changed this situation.

There was less of a gap in LED experience between set makers and panel makers, and LED performance and operation were better understood by set makers than the performance and operation of CCFLs. As a result, LED backlighting successfully accelerated the open-cell business. Panel makers clearly had reason to be concerned about the open-cell model, as they realized that it reduced the value of the product they delivered, and some resisted in providing such panels. However, the panel surplus that developed in mid-2010 forced some panel makers into the open-cell model because they needed to supply open-cell panels in order to maintain business with set makers that requested them for their LED-backlight models.

Another factor was that the slowdown in demand during 2011 resulted in large LCD inventories. Because LCD modules are custom products (mainly due to the backlights), inventories for different customers are not interchangeable, so panel makers have had difficulty reducing inventories. Open cell models have wider compatibility than LCD modules, thus they create the potential for better inventory control, which can help improve the profitability of panel makers. Thus, some panel makers determined that the open-cell model could benefit them and, as a result, have even been increasing open-cell CCFL-backlit panels.

How LEDs Are Changing TV-Set Design

The earliest LED backlight designs used direct lighting, in which a large number of LEDs are mounted behind the display. These failed to gain market share due to high cost, despite their excellent image quality and ability to perform local dimming. Samsung moved to adopt edge-mounted LED backlights and had significant early success, in large part due to the fact that the edge-lit LED backlights enabled extremely thin set designs, in some cases less than 10 mm.

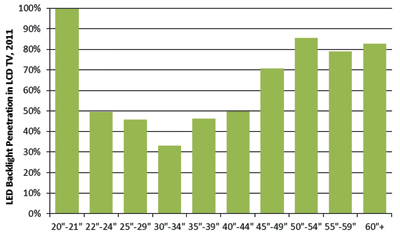

Edge-lit LED backlights allow the set maker to reduce the number of LEDs by concentrating them along the edges. This happened first on all four edges, then moved to two and eventually to a single short edge. Set makers have continued to struggle with an LED premium that many consumers are unwilling to pay for and with continuing rapid erosion of retail prices. In 2011, LED-backlit units accounted for 46% of LCD TVs (Fig. 2).

Fig. 2: In 2011, the share of LED backlights used in LCD TVs reached 46%, but the penetration was lowest in the highest volume size, 32 in. Source: DisplaySearch, Quarterly Advanced Global TV Shipment and Forecast Report.

In 2012, set makers are introducing a new, low-cost direct LED backlight design, targeting CCFL designs with similar thickness and cost (although lower brightness) in the key 32-in. size. Bigger LED emitter chips are used, but in fewer numbers. In some cases, the LED packages include a lens structure on their surface to improve optical performance.

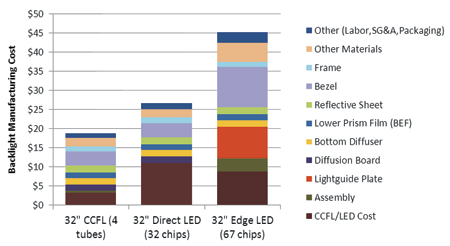

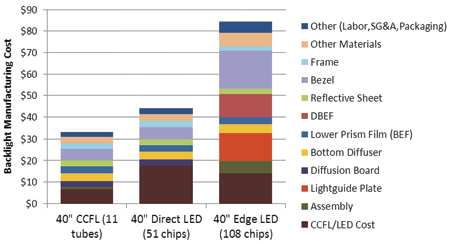

While they require brighter and thus more expensive LEDs, these new designs eliminate the need for the light-guide plate (LGP) and diffuser used in edge-lit designs and for brightness-enhancement film. By running at lower brightness, they can approach cost parity with CCFL backlights (Fig. 3). However, these sets are thicker than edge-lit varieties. In many markets, LED-backlit LCD TV has become associated with slim designs, so thicker set designs could run the risk of confusing consumers.

Fig. 3: New, low-cost direct-lit LED backlight designs for LCD TVs are expected to be close to the manufacturing cost for equivalent CCFL backlights, as shown for 32-in. (top) and 40-in. (bottom) sizes. These designs are significantly cheaper than the edge-lit designs, due to the elimination of the light-guide plate as well as light-enhancement films and reduction in mounting and assembly costs for 40-in. units. Source: DisplaySearch, DisplaySearch Quarterly LED & CCFL Backlight Cost Report.

Ultimate Impact of LEDs on the LCD Industry

The introduction of LED backlighting has changed the pricing, value chain, and structure of the LCD industry, as well as influencing LCD-TV product designs and marketing. The LED has brought significant performance improvements to LCD TV, enabling it to stem the growth of plasma TV and putting it in a good position to compete with OLED TV. But LEDs have also contributed to the shift in power in the industry, as panel manufacturing moves to more of a foundry business model.

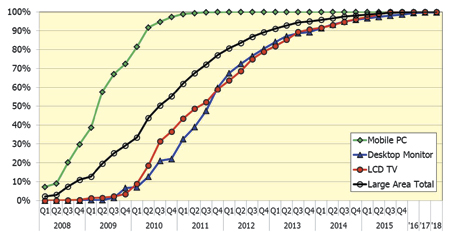

Regardless of the changes in industry structure, LED backlights are now on a path to dominate all LCDs used in PCs and TVs (Fig. 4), particularly as manufacturing costs for LED chips continue to fall and environmental regulations banning the mercury found in fluorescent tubes take force in more countries. The long-term challenge for LED backlights will be to optimize the efficiency of converting point sources to area lighting. •

Fig. 4: After passing 50% penetration of the LCD-TV market in the second half of 2011, LED backlights are expected to increasingly dominate large-area (9.1-in.-diagonal and larger) LCD backlights, with adoption by LCD monitors now growing rapidly. Source: DisplaySearch Quarterly LED & CCFL Backlight Cost Report.

Paul Semenza is Senior Vice-President, Analyst Services for DisplaySearch. He can be reached at paul.semenza@displaysearch.com. Jimmy Kim is Senior Analyst, Display Materials and LEDs, at DisplaySearch.