OLEDs in Transition

The OLED industry is in the midst of change – from passive to active matrix and from small to larger sizes. This change is being driven by a significant amount of investment in active-matrix OLED manufacturing facilities – with the ultimate goal being to compete in the TV market. While the industry attempted to commercialize OLED TV in the past, the cost structure and productive capacity were not ready. This time, the pieces are coming together for a successful market entry.

by Paul Semenza

IN 2011, total organic-light-emitting-diode (OLED) display shipments are expected to reach 180 million units, which represents a growth rate of 61% over 2010. Unit growth is being driven by active-matrix OLED (AMOLED) display shipments, whose growth rate increased from 103% in 2010 to 136% in 2011, while passive-matrix OLED (PMOLED) display shipment growth fell from 20% to 9%. AMOLED-display growth is expected to again surpass 100% in 2012, as AMOLED-display manufacturing capacity undergoes significant expansion. After almost doubling in 2010, total OLED-display revenues are expected to nearly triple in 2011, reaching $4.5 billion. Revenues are expected to more than double in 2012 and to exceed $20 billion by 2016. Even more so than in the case of units, active matrix dominates OLED-display revenue growth. Driven by unit growth as well as increases in average screen size, AMOLED-display revenues will grow more than tenfold between 2010 and 2013, from $1.25 billion to $12.9 billion. Growth in PMOLED-display revenues has been slowing and is likely to peak by 2015 at just over $400 million, as active-matrix LCDs (AMLCDs) and OLED displays take share from passive matrix.

Mobile Phones a Successful Platform for AMOLED Displays

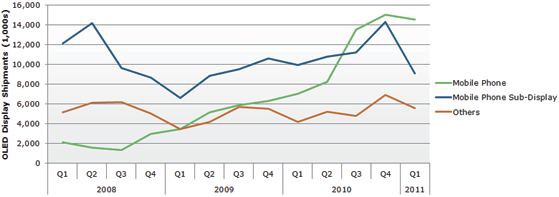

Mobile-phone displays remain the core application for OLED displays, but the composition is shifting from secondary to primary displays as AMOLED displays have entered mass production, and as flip (or clamshell) type phones continue to lose share to larger, single-display smartphones (Fig. 1). Samsung-branded smartphones have been the dominant application for AMOLED displays. The display size has increased from 3.3 to 4.0 in. in 2010 models to 4.0 to 4.5 in. in 2011 models. At the IFA show in Berlin in September, Samsung showed its new Galaxy Note smartphone, having a 5.3-in. AMOLED display. Nokia also expanded its AMOLED-display product portfolio in 2011, with six smartphone models using AMOLED displays between 3.5 and 4.0 in.

Fig. 1: Mobile-phone main displays have emerged as the leading application for OLED displays, as the market has shifted to smartphones and away from flip phones, and as AMOLED-display production has ramped up. Source: DisplaySearch Quarterly OLED Shipment and Forecast Report.

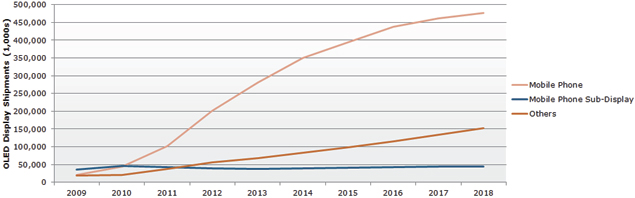

The next promising application for AMOLED displays is the amusement market, including portable game machines. There are high expectations for PSP Vita, the new portable game machine with AMOLED displays that Sony recently announced. AMOLED displays for PSP Vita are expected to start shipping in Q3 '11. In the digital-still-camera (DSC) market, another promising application for AMOLEDs, shipments started to increase in Q4 '10. However, as can be seen in Fig. 2, on a unit basis, no other application is expected to come close to mobile-phone displays as a source of demand for OLED displays.

Fig. 2: Mobile-phone main displays will continue to represent the largest application for OLED displays in unit terms. Source: DisplaySearch Quarterly OLED Shipment and Forecast Report.

The main application for PMOLED displays, mobile-phone sub-displays, has been stagnant because of the surging popularity of smartphones without sub-displays. Japanese PMOLED-display suppliers, such as TDK and Pioneer, have decreased sub-display shipments, while Taiwanese and Chinese PMOLED-display makers are increasing shipments for home appliances and other applications.

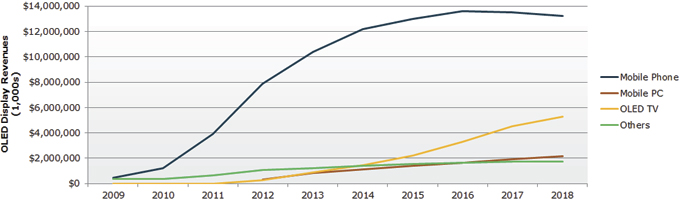

The rapid growth of mobile-phone displays will be the primary driver behind OLED-display revenue growth for the next few years (Fig. 3). After 2014, lower unit growth and expected price declines will result in a slowdown in revenue growth. At that point, we expect to see TV emerge as the key driver of revenue growth for OLED displays. While expectations are high for OLED TVs in the near term, it will take a few years for advanced-generation AMOLED-display factories to come on line, increase yields, and drive down costs. Along with the ability to make 30+ in. TV panels, these new factories will also enable mass production of 5–15-in. panels for mobile PCs. It is possible that we could see tablet PCs with AMOLED displays commercially available in 2012. At the IFA Conference, Samsung showed a Galaxy Tab with a 7.7-in. AMOLED display, but withdrew the sample during the tradeshow.

Fig. 3: Mobile-phone main displays will dominate revenues for OLEDs for the next few years, but after 2014, revenues from TV will grow much faster, and mobile PCs will also become a significant application. Source: DisplaySearch Quarterly OLED Shipment and Forecast Report.

Market Growth Driven by Production

In 2010, Samsung Mobile Display (SMD) shipped 45.6% of all OLED displays and 99.3% of AMOLED displays; in the first quarter of 2011, SMD increased its share of shipments to 51.5% and 99.9%, respectively. Because of the company's lead in the higher-value AMOLED technology, Samsung increased its share of revenues from 81.3% in 2010 to 88.3% in Q1 '11. It is rare in the display industry to see anywhere near this level of dominance by one company in a technology category. There is the possibility that a first-mover advantage exists in AMOLED technology: depreciation as a share of total cost is approximately twice that of TFT-LCDs, meaning that the first to fully depreciate capital expenditures will have a significant cost advantage. However, given the fact that Samsung is vertically integrated in mobile phones, TVs, and other products, some OEMs are reluctant to adopt AMOLED displays as long as SMD has such dominance. So, in order for the OLED-display market to grow significantly, other suppliers are clearly needed in the market.

For the next few years, however, SMD is likely to continue to be the leading supplier of OLED displays. The company started mass production at the first Gen 5.5 AMOLED fab in June 2011. It is expected to expand its Gen 5.5 AMOLED-display lines and ramp-up Gen 8 lines for large-sized AMOLED panels. AMOLED panels for mid- or large-sized applications, such as mobile PCs and OLED TVs, are forecast to start shipping in 2H '12 when SMD expands its production capacity or ramps up large-sized AMOLED-display production, although technical uncertainties remain both in backplane design and organic materials deposition.

After suspending production in the middle of 2010, LG Display (LGD) is planning to resume AMOLED-display production on its Gen 4 line and was expected to restart shipping AMOLED displays for mobile phones in Q2 '11. However, LGD's main focus for AMOLED displays is the TV market. It is planning to ramp up a Gen 8 AMOLED-display fab in 2012. The company has been pursuing white OLEDs with color filters rather than RGB emitters and is developing IGZO-based white AMOLEDs with color-filter–on–TFT technology.

In Taiwan, AUO and CMI have smaller fabs (Gen 3.25) that are in mass production or are planned to be in 2012; these fabs are limited to producing mobile phone and other small-to-medium displays. AUO is also preparing its Gen 4 fab in Singapore to produce AMOLED displays.

In China, IRICO is building a Gen 4 AMOLED-display fab in Foshan-Shunde, which could begin mass production in late 2012. On August 12, the BOE Group made a surprise announcement that it will invest $3.5 billion to build a Gen 5.5 AMOLED-display production line in Ordos, a city in the Gobi desert in China's Inner Mongolia Province, in exchange for rights to extract coal from the resource-rich province. It will be a significant challenge to operate an AMOLED-display fab in such a remote location, without any supply chain or plentiful water supply, and for BOE to make the leap into Gen 5.5, the leading edge of AMOLED-display production.

All of the Japanese producers of AMOLED displays have exited the market or stopped production, including, most recently, Sony, although the company still has some capacity. Ortus, a joint venture of Toppan Printing and Casio, has also been developing pilot production for AMOLED displays. Other Japanese companies that have historically had development or produced AMOLED displays include Epson, Hitachi, Panasonic, Sanyo, Sharp, and Toshiba.

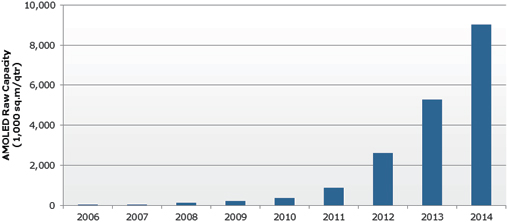

Taking all of these developments into account, it is clear that there will be a significant increase in overall AMOLED-display manufacturing capacity (Fig. 4). This is a crucial development for the industry, as it will give customers the confidence to adopt the technology and allow for multiple applications to be pursued. It will also provide the experience needed to tackle the significant challenges in scaling to larger substrate sizes.

Fig. 4: Led by Samsung Mobile Display (SMD), AMOLED-display manufacturing capacity is expected to grow tenfold over the next 4 years, as the industry moves beyond Gen 4 fabs. Source: DisplaySearch Quarterly FPD Supply/Demand and Capital Spending Report.

Ongoing issues for scaling AMOLED-display production beyond the existing Gen 4 lines center on backplane manufacturing and organic material deposition.1 The latter can be addressed by creating the backplane on a full substrate and then cutting the substrate into smaller pieces for organic materials deposition. For the backplane, most of the focus has been on low-temperature polysilicon (LTPS), but the challenges of scaling this technology beyond Gen 4 have led to continued development of alternative technologies such as oxide semiconductors. In addition, work continues on using a-Si TFTs, the dominant form of active-matrix backplane technology, in AMOLED displays. At SID 2011, IGNIS and RiTdisplay demonstrated a-Si TFT AMOLEDs, using architectures and technologies developed by IGNIS.

In PMOLED-display manufacturing, RiTdisplay, SMD, Pioneer, and TDK were the original market leaders, but SMD moved its focus to AMOLED displays at the end of 2010, and Pioneer has been losing share as demand in mobile phones and automotive markets has been declining. At the same time, WiseChip, which acquired Univision's OLED business, took the lead in the first quarter of 2011, and Visionox has been steadily increasing its market share; both companies have had success with mobile phones for Asian markets, as well as appliances and other applications.

This Time, Will Things Be Different?

The OLED-display market has suffered from an excess of hype and a deficit of real products. From picture frames to TVs, products have been introduced without the ability to produce them in volume at a cost that would allow them to compete with TFT-LCDs. At the same time, the incumbent technology has been improving, using LED backlights to reduce thickness and improve color gamut, as well as novel pixel architectures to improve viewing angles. Thus, OLED displays face a more challenging competitive environment than a few years ago. Why might things turn out differently this time?

The biggest factor is the ongoing investment in AMOLED-display manufacturing. The demand for displays is huge and growing – in 2010, OLED displays represented just over 0.1% of the total display market, measured by area. The challenge for AMOLED displays has been to build out manufacturing capacity that would allow the technology to serve multiple applications, particularly the key large-area products: mobile PCs, desktop monitors, and TVs. To date, there has been a "chicken-and-egg" problem – given the relative immaturity of OLED technology, its cost structure is higher, but given the competitive nature of the computer and consumer electronics markets, AMOLED technology needs to be competitive with TFT-LCD pricing.

At the same time, the inherent simplicity of OLED technology and the small amounts of materials needed for manufacturing strongly suggest that OLED displays should be cheaper to produce in high volumes. But it still takes a first mover to invest in state-of-the-art production and to work with equipment suppliers to surmount the barriers to large-sized AMOLED-display production. What we are seeing at present is a combination of market acceptance in mobile devices, combined with the beginning of a sustained series of investments. If realized, these investments will enable OLED-display technology to make the transition to a mass-market display technology.

References

1For a discussion of developments in AMOLED-display manufacturing, see P. Semenza, "Can OLED Displays Make the Move from the Mobile Phone to the TV?" Information Display 7&8 (2010). •

Paul Semenza is Senior Vice-President, Analyst Services, with the market research firm DisplaySearch. He can be reached at