A New Chapter for the Display Market

The Great Recession of 2008–2009, combined with maturity in key market segments, has moved the display industry into a new, slower growth phase. The impacts are already being felt.

by Paul Semenza

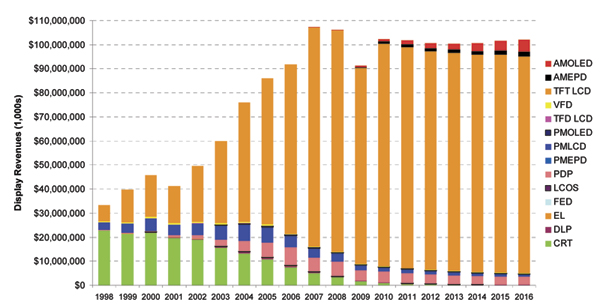

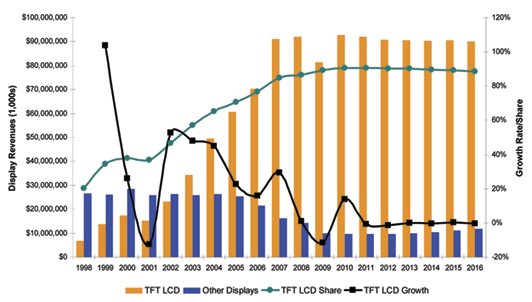

THE DISPLAY MARKET has gone through several stages of growth. As detailed in Figs. 1 and 2, the market grew rapidly over the past decade, driven by expansion in TFT-LCD production. What had been until the late 1990s a relatfively small industry focused primarily on the growing notebook-PC market expanded dramatically, first into desktop-PC monitors and then into televisions. In both cases, the advantages of TFT-LCD technology over the incumbent CRT technology were quite obvious, with improvements in volume, weight, potential screen sizes, and resolutions, and, eventually, in image quality.

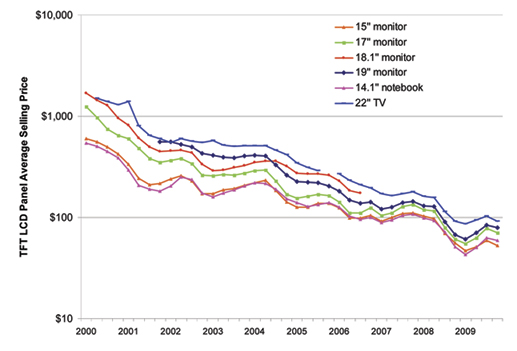

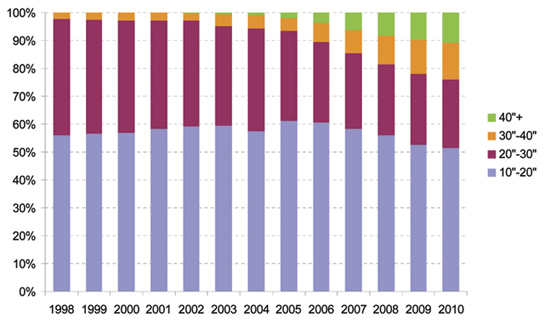

The challenge was in bringing the price down to an acceptable level, which was achieved through massive investments in successive generations of TFT-LCD manufacturing and in the materials and equipment that round out the supply chain. These investments led to significant declines in price, as well as dramatic increases in screen sizes (Figs. 3 and 4).

However, as Figs. 1 and 2 indicate, after growing rapidly throughout the 2000s, industry revenues declined in both 2008 and 2009. While the immediate cause of this decline was the global recession, the display industry has also entered a mature phase. With notebook PCs and desktop monitors completely penetrated by TFT-LCDs, much of the growth in recent years has come from the TV market. Despite the recession, flat-panel-TV shipments grew on the order of 30% per year in 2008 and 2009. However, this growth is leading to high penetration rates, even in formerly emerging markets, such as China, and will push the flat-panel share of the TV market past 90% in 2011. This high penetration, combined with increasing pressure on prices, will lead to slower revenue growth, particularly for TFT-LCDs.

New Market Conditions Drive Consolidation

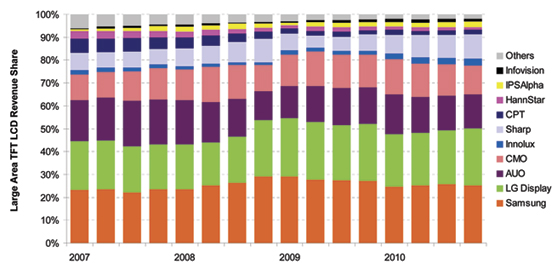

In key areas of the display industry, there is an ongoing trend toward increased consolidation. In the large-area TFT-LCD market, five panel makers now dominate revenues (Fig. 5).

This has come about through aggressive investments and mergers. There are now two large TFT-LCD manufacturers in Korea (Samsung and LG Display), two in Taiwan (Chimei Innolux and AUO), and two in Japan (Sharp and Panasonic, which owns IPS Alpha). For plasma manufacturers, there are three major producers (Panasonic, Samsung, and LG Electronics), and in active-matrix OLED-display manufacturing, Samsung Mobile Display has a commanding share of the market. Even in small-to-medium displays, a category that has traditionally been fragmented due to the customized nature of the products, there is increasing concentration, with TPO, a low-temperature-polysilicon (LTPS) manufacturer, now part of Chimei Innolux. Japanese panel makers, traditionally the leaders in small and medium displays, are scaling back, as exemplified by Epson, Hitachi, NEC, and Toshiba.

Fig. 1: Display revenues grew rapidly in the 2000s, as TFT-LCD technology displaced lower-cost technologies in television, computing, and communications applications. However, display revenues fell in 2008 and 2009, and while growth is expected to resume in 2010, it is not clear when revenues will surpass 2007 levels. All charts courtesy DisplaySearch.

Fig. 2: The early growth phase of the TFT-LCD market following the financial crisis of 1998 was curtailed by the dot-com crash. The CRT-replacement period of 2002–2007 was marked by very strong growth. The recession of 2008–2009 coincided with a high level of saturation of TFT-LCDs in key markets: TV, desktop monitors, notebook PCs, and mobile phones. 2010 is likely to be the start of a period of maturity, with slow growth.

Going forward, there are likely to be significant investments in TFT-LCD manufacturing in China, but whether this reduces concentration depends upon the nature of the companies making the investments. In some cases, they may be wholly or partially owned by Taiwanese, Korean, or Japanese panel makers. In addition, the plants in China are likely to be limited to Gen 8 for several years, due both to restrictions on technology transfer by foreign governments, but also due to the focus on cost reduction for 20–40-in. screen sizes, rather than a continued push to the upper limits of screen size. It may be some time before any company joins Sharp at Gen 10 or larger-sized substrates. The basis for competition will be shifting from having the largest fab to being the first to address emerging applications and having the lowest manufacturing cost and the most efficient supply chain.

Pursuing Premium Markets

With continuing price pressure, it is increasingly important for display makers to capture any opportunity to charge a premium price. The most common approach is to exploit a new technology or feature and be the first mover. The move to LED-backlit LCDs for TVs is an ongoing example of this; at both the panel and set level, there were healthy margins for such products in 2009. As the LCD-TV market rapidly adopts LED backlights, such premiums will erode. The next hope for premium pricing is 3-D TV, in whichhigh-frame-rate (120 Hz and higher) panels can be used in conjunction with additional video-processing electronics and shutter glasses to produce a premium product. Display makers can add more value to their products in other ways as well; for example, by integrating touch or other forms of inter-activity.

Reducing Manufacturing Costs

Much of the cost reduction over the past decade has been driven by investment in TFT-LCD factories. Larger substrates, higher throughput equipment, and the learning that comes from cumulative production have driven down the cost of producing the LCD "cell" – the TFT array and color-filter plates combined with the liquid-crystal layer and polarizers. The success of these efforts to drive down costs has put a spotlight on other aspects of display manufacturing; in particular, the backlight. The conventional CCFL tubes used in backlights are very mature and thus do not have a high rate of cost decline. In large panels, the backlight can account for 25% of manufacturing cost.

Fig. 3: The prices of TFT-LCD panels fell by a factor of 10 during the 2000s.

There are two broad approaches to lowering the backlight cost: reducing the cost of the light sources and improving the efficiency of the panel, thus requiring less light to be produced by the backlight. The first approach has involved moving from CCFL to LED sources. While initially more expensive than CCFL backlights, LED backlights are rapidly declining in price, driven by a massive increase in LED chip production, which results in lower costs and higher efficiencies. In addition, LEDs are enabling the use of new backlight designs that have the potential for lower costs. Improving optical transmission has involved innovations in the array, color filter, and cell processes.1

Fig. 4: The expansion in TFT-LCD manufacturing capacity has led to rapid growth in 30-in. and larger panels.

Vertical Integration

There is a great deal of vertical integration in the LCD-TV supply chain, from panel makers vertically integrating more LCD components to LCD-TV set makers vertically integrating LCD-module assembly. LCD-TV set makers, especially in China, have started to invest in LCD-module assembly lines. Due to a lack of experience with LCD-module processes, most are working with panel makers, and in many cases have formed joint ventures. For example:

• Skyworth has invested in LG Display's LCD-module factory and established its own LCD-module assembly line.

• Hisense and Konka have set up LCD-module assembly lines with the help of CMO; TCL set up an LCD-module assembly line using know-how transmitted from Samsung.

• AUO and Changhong jointly invested in an LCD-module line.

• LG Display formed an alliance with AmTRAN to set up an LCD-module and LCD-TV-set assembly line and set up a joint venture with TPV for LCD-module lines.

• AUO and TPV are jointly establishing an LCD-module line in Eastern Europe.

An extension of vertical integration is "module in backlight," which refers to the integration of LCD modules and backlights. As more LCD-TV makers enter LCD-module assembly and gain experience, they are finding that they can take on another labor-intensive process: backlight units. Some backlight suppliers have also set up their own LCD-module lines and penetrated the LCD-module assembly business. Re-engineering efforts help to create a compact design, which can reduce components. The ultimate trend is total integration. Since there are many similarities between the LCD module and the TV chassis, companies will begin to integrate these. In the future, panel makers may just ship the cell to an integrated assembly line, which will assemble a hybrid module consisting of an LCD module, backlight, bezel, and LCD-TV chassis, and turn out a complete LCD-TV set. The supply chain lead time would be significantly reduced for faster entry into the market.

Fig. 5: Concentration in large-area TFT-LCD revenues has been increasing. With the Chimei– Innolux merger, the top five panel makers account for more than 90% of revenues.

Looking Ahead

With the key markets in mobile devices, PCs, and TVs converted to high-performance flat-panel displays, the display industry will likely be entering a period of slow revenue growth, even as there is continued unit growth in TV, portable computing, and mobile devices. The ongoing trend of consolidation and focus on manufacturing efficiency is a logical reaction to the market conditions. Looking forward, we can expect new applications to emerge as drivers of revenue growth, particularly as cost savings are reflected in market pricing. Such applications could address a variety of markets, including public displays, as the cost of large-area displays drops; electronic reading devices, as flexible and lightweight displays become available; and "re-usable" displays, for applications such as restaurant menus and performance playbills.

References

1C. Annis and P. Semenza, "Better Transmission: TFT LCD Manufacturing Advances Reduce Cost and Energy Consumption,"Information Display 12 (December 2009). •

Paul Semenza is Senior Vice President, Analyst Services, with DisplaySearch. He can be reached at paul.semenza@npd.com.